Debt sustainability in fragile and conflict-affected states: heightened risks and needs

Debt sustainability in fragile and conflict-affected states: heightened risks and needs

Fragile and conflict-affected countries face a daunting reality of critical spending needs and heightened exposure to shocks. International support can help relieve debt distress by enhancing fiscal management.

This blog is part of the series Learning from Fragility that aims to inform discussions at the upcoming Fragility Forum by exploring lessons from past support for development in fragile and conflict settings.

Although debt vulnerabilities are increasing among all low-income countries, the particular challenges facing those affected by fragility and conflict exacerbate these vulnerabilities. In addition to heightened risks in the face of shocks that could drive otherwise solvent countries into debt distress, those in fragile and conflict-affected situations (FCS) also struggle significantly more to ensure critical spending for stability and long-term development needs.

Challenges also include the need for considerable infrastructure spending and other public investments for reconstruction; limited fiscal space due to security-related expenses or inability to mobilize resources in areas outside of government control; and decreased private sector development due to greater uncertainty and limited rule of law. These circumstances make robust public financial management and public debt management all the more urgent in FCS countries.

A worrying trend of debt distress among IDA countries

A recent IEG blog on an Early Stage Evaluation of the Sustainable Development Finance Policy of IDA, the World Bank’s fund for the poorest countries, highlighted some important findings about the risk and the rapidity with which low-income countries can fall into debt distress. First, between 2013-2021, the number of IDA eligible countries which either moved to high risk of debt distress or fell into debt distress tripled, from 13 to 36. As importantly, the speed at which countries moved into debt distress was alarmingly high.

Among the countries which experienced a deterioration in their debt distress risk level, one-third experienced a two-level increase (from low to high, or from moderate to in debt distress) in the span of fewer than three years. Countries that exhibit seemingly low levels of debt distress risk can see startlingly quick changes of fortune.

The exceptional risks for fragile and conflict-affected situations

What is less appreciated is the more sizeable risks for FCS countries. A notable difference between IDA-eligible countries classified as fragile and conflict-affected situations and IDA-eligible countries that are not is the speed with which their ability to service their debt can change.

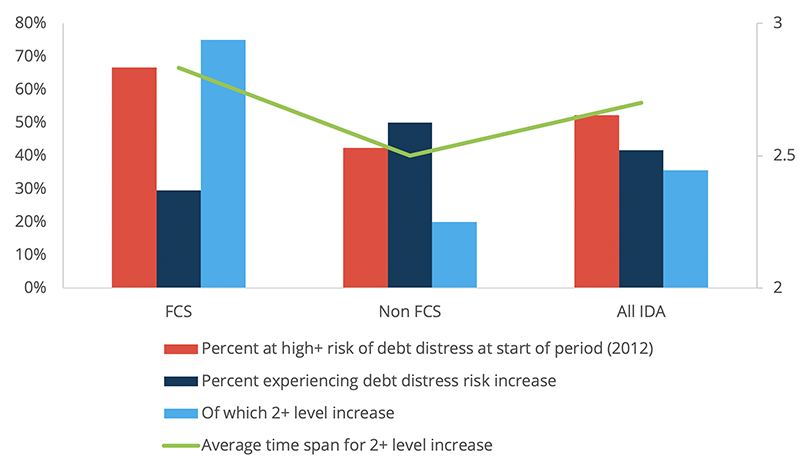

Between 2012-2020, about a third of FCS countries experienced some deterioration in their risk of debt distress (this seemingly low number belies the fact that, at the start of the decade, a third of FCS countries were already at high risk of or in debt distress). Of the FCS countries which saw a rise in debt distress risk, fully three-quarters of them experienced a two-level increase or higher over less than three years. The comparable figure for non-FCS countries over the same period was 20% (see Figure 1).

Figure 1: Risks and speed of debt distress risk deteriorations, FCS versus non-FCS IDA-eligible countries (2012-2019)

Source: IEG staff calculations from IMF/World Bank Debt Distress Risk ratings database. Note: 2+ level increase reflects increase in assessed risk of debt distress from low to high, or from moderate to "in debt distress."

Why are fragile countries so vulnerable to falling into debt distress?

The 2017 Joint World Bank/IMF Review of the Debt Sustainability Framework highlights several reforms to improve the reliability of debt risk assessments. This review did not specifically look at differences between FCS and non-FCS countries. However, several factors which influence debt carrying capacity may explain the significantly greater risks for rapidly deteriorating debt distress among FCS countries:

To begin with, FCS countries are disproportionately vulnerable to downward-oriented growth shocks, which impact debt and debt service/GDP ratios. While IDA-eligible countries as a whole exhibit considerable volatility in growth, growth downturns (year-on-year deteriorations in growth) are significantly more common among FCS.

In addition, when such GDP growth downturns occur, the magnitude of the downturn is significantly greater for FCS. Over the period 2011-2019, the median growth decline for non-FCS countries was about 36% (that is, during years of growth downturns, the growth rate in the downturn year was about 36% less than the year prior). For FCS, the median growth rate downturn over the downturn year was over 100%—meaning that, for FCS countries, most downturns reflected growth falling to zero or actual declines in real GDP.

Other factors important for debt carrying and debt service capacity likely to disproportionately impact FCS countries include weaker institutions (which can contribute to underestimation of public debt), more limited debt rollover capacity, greater likelihood of capital flight, and poorer fiscal outturns, which impacts spending on basic social services.

Public expenditure management in FCS countries is critical

In the face of both higher risks of shocks as well as heightened critical spending needs, World Bank support to buttress debt sustainability among FCS countries should pay particular attention to enhancing fiscal management.

While sound public expenditure management (PEM) is important in all countries to avoid wasting scarce resources, the criticality of improving public expenditure efficiency in FCS countries is unparalleled.

Beyond the need for countercyclical spending for stabilization, FCS countries need to direct public spending to areas critical to escape fragility traps. For example, a recent IMF blogon escaping fragility notes that countries that successfully exit fragility spend more on health and education than those that do not escape. Protecting social spending enhances social inclusion and stability, which are often critical to address drivers of fragility. And when resources are scarce there is a need for greater attention to public expenditure efficiency.

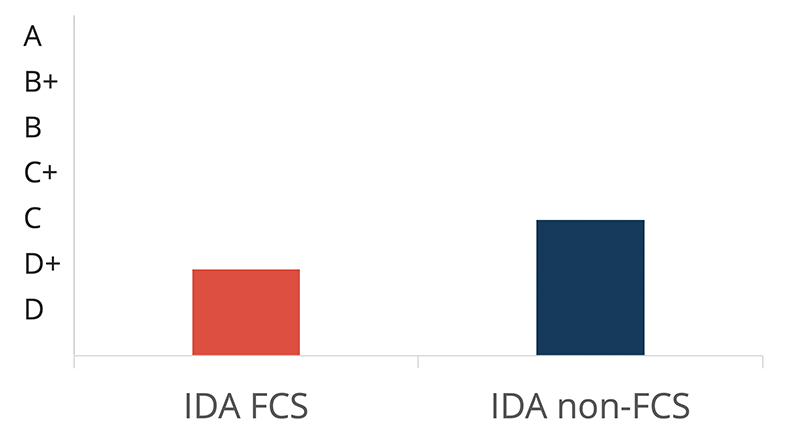

Public investment management is also an important part of the equation, particularly when reconstructing following political crises or conflicts. With varying capacities to identify and design quality investments and effectively manage their implementation, many investments in FCS countries fell far short of growth aspirations. The average PEFA public investment management indicators score for the 24 FCS countries with 2016 framework data is D+, compared to a C for the 37 non-FCS countries (Figure 2).

Figure 2: Public Investment Management (PIM) Capacity in FCS vs. non-FCS IDA Countries

Note: This indicator assesses the economic appraisal, selection, costing, and monitoring of public investment projects by the government, with emphasis on the largest and most significant projects. The average in red includes all IDA-eligible countries that were classified as FCS at least once (2010-present). The data used is from the latest PEFA report available and the numerical conversion of PEFA scores was conducted usingPEFA Secretariat’s crosswalk methodology.

FCS countries face the daunting reality of critical spending needs and increased exposure to shocks that easily can throw otherwise stable countries into debt distress. This means that the World Bank's increased focus on debt vulnerabilities should pay particular attention to both the disproportionate risk factors facing FCS countries as well as the public expenditure management and public investment management systems needed to properly mitigate some of these risks.

Add new comment