Why is it so hard to raise taxes in developing economies? Lessons from World Bank Experience with Domestic Revenue Mobilization

Why is it so hard to raise taxes in developing economies? Lessons from World Bank Experience with Domestic Revenue Mobilization

A new evaluation from the Independent Evaluation Group assesses the impact of World Bank support for Domestic Revenue Mobilization and identifies lessons for turning increased attention to this critical source of financing into sustained progress.

In 2015, at the World Conference on Financing for Development in Addis Ababa, the international development community recognized that official development assistance was unlikely to be adequate to achieve the ambitious Sustainable Development Goals, and resources from other sources would be needed, including domestic revenue mobilization (DRM). The World Bank was among the multilateral institutions that committed to step up its support for this critical source of financing, pledging to ramp up its support to client countries.

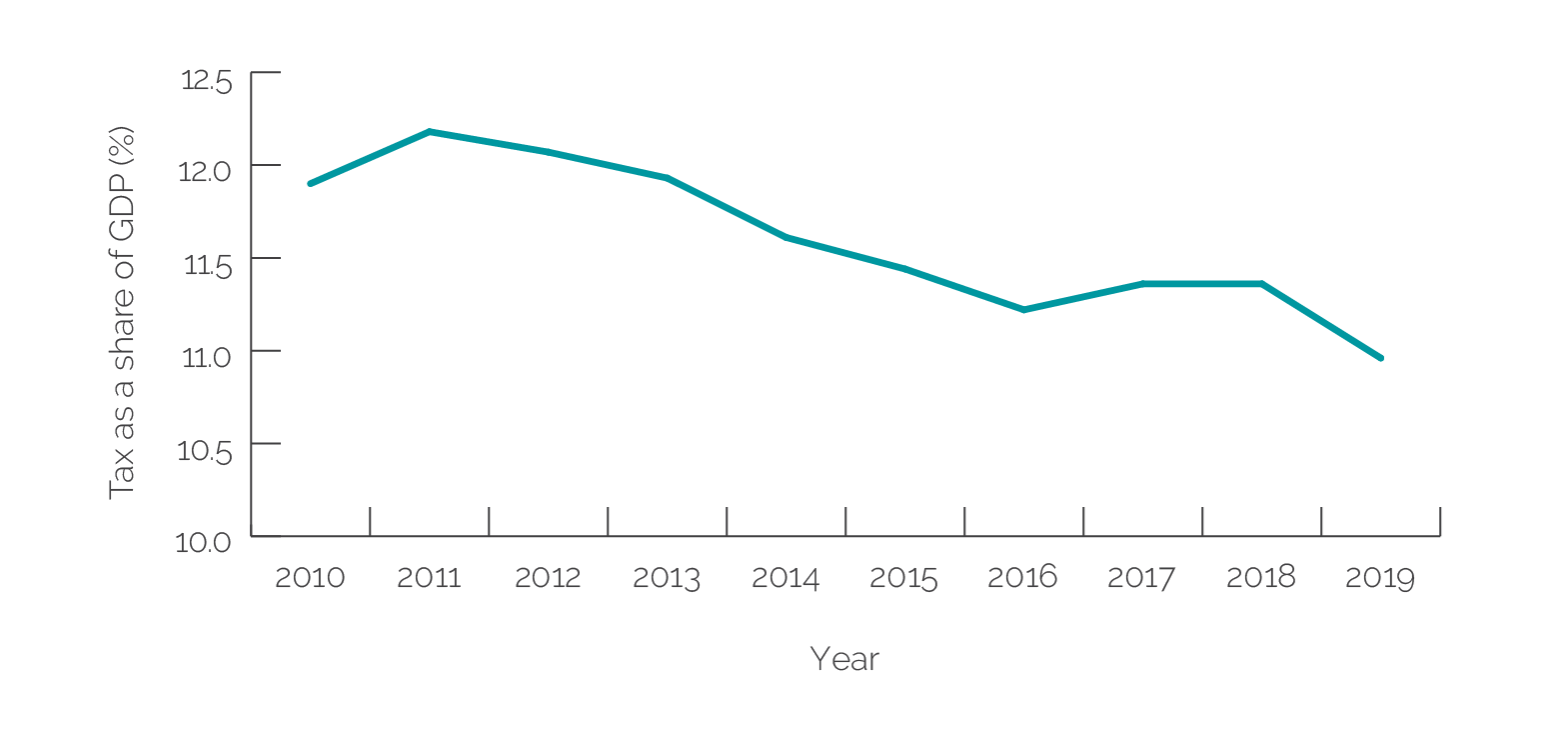

But despite increasing attention on DRM, tax yields have been on a declining trend over the past decade. A reversal of the trend in 2016 was short lived, peaking in 2018 at 11.4% of GDP, declining sharply to 10.9% in 2019. At the same time, high fiscal deficits and already high and rising debt levels in the years leading up to the COVID-19 pandemic made enhancing DRM a significant priority for developing economies, particularly lower-income countries. Since the onset of the pandemic, tax revenues have dropped by 12% in real terms, and in many countries, ratios of tax to gross domestic product have fallen below 15% —considered the minimum necessary to finance a state’s basic functions.

Tax as a Share of Gross Domestic Product in Low- and Middle-Income Countries

Source:World Development Indicators database. Note:GDP = gross domestic product.

World Bank support for domestic revenue mobilization in the period following the 2015 World Conference on Financing for Development and leading up to the COVID pandemic was the subject of a recent Independent Evaluation Group (IEG) evaluation. The evaluation confirmed that the World Bank had intensified its DRM work, particularly since 2018 and especially to countries eligible for IDA, the World Bank’s fund for the poorest countries, and to Sub-Saharan Africa. The increase in support was greatest in countries with lower ratios of revenue to GDP.

Much of the increase in attention to DRM was in the form of analytical work, largely supported through the Global Tax Program (GTP), a multi-donor trust fund established in June 2018. While GTP funding allowed the World Bank to increase its analytical support for DRM, it also intensified pressure on limited staff and an increasingly large cadre of short-term consultants. Significant turnover in staff and management working on tax issues exacerbated these pressures, along with several shifts in responsibility for tax within the World Bank Group.

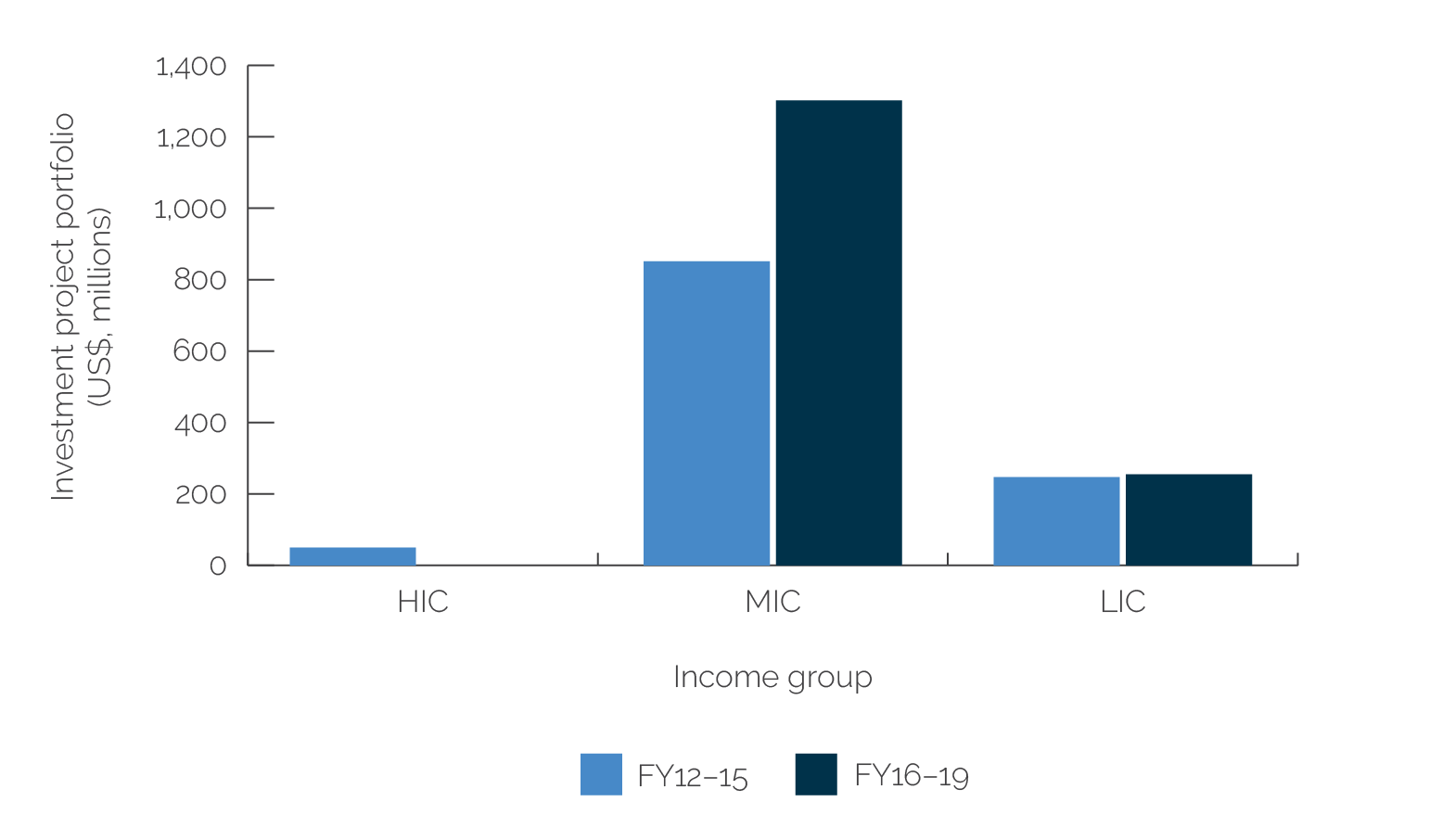

World Bank investment projects – largely to improve tax administration – rose (relative to the previous 3-year period) but the increase was almost entirely concentrated in middle-income countries, and largely due to a small number of large projects in South Asia. There was little growth in investment lending to low-income countries to support tax administration. That said, results from these projects were generally favorable with the share rated satisfactory at 41%, with 35% of projects rated moderately satisfactory.

Investment Project Portfolio by Income Level, FY12–15 and FY16–19

Source: World Bank Business Intelligence database, May 2021.

Note: FY = fiscal year; HIC = high-income country; LIC = low-income country; MIC = middle-income country.

The increase in attention to domestic revenue mobilization was most evident in World Bank budget support operations, also known as development policy operations (DPOs). The number of DPOs approved with at least one DRM-related prior action increased from 65 to 84 between FY12–15 and FY16–19 (rising also as a share of DPOs from 27% to 42%). These tended to focus on reforms to tax policy. The increase was most pronounced in lower income countries. In total, there were 133 DRM-related budget support operations across 54 countries, up from 112 DRM-related budget support operations across 36 countries in the previous period.

Evaluation findings showed that targets for a significant majority of DRM-related results indicators in DPOs were achieved during the evaluation period. However, indicators used to measure impact were often too high level or did not adequately capture either the impact of prior actions or progress toward objectives. This undermined their value as measures of impact, reducing opportunities for course correction and learning from experience.

Case studies from the IEG evaluation on DRM as well as an Evaluation Insights Note (EIN) on Tax suggest that results from DRM policy reforms supported by DPOs were often not sustained. Even for operations that recorded significant achievements at closing, progress was frequently reversed over time because of policy reversals. This was particularly the case for efforts to address the proliferation of tax expenditures or tax exemptions, which accounted for just under one-quarter of DRM-related prior actions in the evaluation period. For example, in Pakistan, after starting to decline in 2014, tax exemptions were reintroduced in advance of 2018 elections, increasing from 1.6 to 2.5% of GDP between 2017 and 2019. As a result, tax collection deteriorated from 12.9 to 11.6% of GDP. In Panama, elimination of tax exemptions proved more difficult than envisioned amid strong political headwinds in domestic tax reform outside the executive branch of government. In Madagascar, the World Bank supported disclosure of a summary of all tax expenditures in the annual budget law, but rather than a targeted reduction of about $24.8 million in tax exemptions, tax expenditures eliminated during the Public Finance Sustainability and Investment DPO series (2016–18) were less than $0.4 million, and in 2017, the government approved additional tax benefits for special economic, industrial, and agriculture zones.

The ease with which some World Bank–supported tax policy reforms can be reversed points to potential tension between the successive provision of budget support to clients that fail to make concrete and sustained progress on DRM. Specifically, the provision of budget financing can reduce how urgently clients approach DRM and the priority they assign to sustaining progress. This suggests that a failure to make and sustain progress on DRM should be considered more explicitly in deciding on the size and frequency of subsequent budget support, at least outside the context of countercyclical support during a crisis.

4 recommendations for enhancing the impact of support to DRM

On a country-by-country basis, regularly take stock of the findings of the broad range of tax diagnostics tools and instruments to (i) identify knowledge gaps and (ii) more systematically inform priority setting for country-level policy dialogue, capacity building, and operations to improve DRM. The outcome of this exercise should be timed and used to inform the design strategies to support individual countries and the conditionality underpinning DPOs.

Given the potentially large and regressive fiscal impact of tax exemptions, the World Bank should regularly assess the effectiveness and efficiency of tax exemptions in achieving country-specific policy objectives, with an eye to more actively supporting the sustainable reduction of regressive tax exemptions through policy advice and conditionality in DPOs.

The frequency with which tax policy reforms are reversed calls for strengthening incentives to sustain reforms and make reversal more challenging. As part of this effort, the World Bank should emphasize reforms to contain the proliferation of new tax exemptions. Where feasible, prior actions should prioritize measures that strengthen the governance framework for granting exemptions.

Given how often shortcomings were identified in indicators intended to track progress on DRM, World Bank staff need more concrete guidance on good practice in defining indicators for tracking the impact of World Bank DRM interventions. This will facilitate learning from experience and strengthen accountability and the outcome orientation of support for DRM.

Add new comment