IFC’s and MIGA’s Support for Private Investment in Fragile and Conflict-Affected Situations

Chapter 2 | IFC and MIGA Engagements in FCS: How Effective Are They?

Highlights

The International Finance Corporation and Multilateral Investment Guarantee Agency have not been able to scale up their business volumes in fragile and conflict-affected situations (FCS), despite the introduction of new instruments and modalities for advisory and investment support to FCS countries.

The International Finance Corporation and Multilateral Investment Guarantee Agency investments and guarantees are concentrated in a few countries that already attract sizable foreign direct investment flows.

Despite the challenging business environment and constraints in FCS, evaluated International Finance Corporation projects perform almost as well as those in non-FCS, especially infrastructure projects and larger investments in larger economies. The Multilateral Investment Guarantee Agency’s projects in FCS performed better than those in non-FCS countries.

This chapter discusses the scale and effectiveness of IFC and MIGA engagements in FCS. It considers the volume of private investment supported by IFC and MIGA in FCS, the evaluated project portfolio’s effectiveness, and the private sector development and broader development outcomes associated with IFC and MIGA engagements. The chapter also explores the implications of a worsening in fragility and of the coronavirus pandemic (COVID-19).

Scaling Up IFC and MIGA Investment Support in FCS

IFC and MIGA have not set specific corporate targets for business volume growth in FCS, but scaling up investments in FCS remains a strategic objective for both institutions. There are no agreed corporate targets for FCS countries to complement those for the low-income country FCS and IDA FCS identified in the capital increase package and in MIGA’s strategy, respectively. IFC has an ambitious commitment of delivering 40 percent of its business volume in IDA and FCS countries and 15–20 percent in low-income IDA and IDA FCS countries by 2030. MIGA committed to increase the share of the volume of guarantees issued to projects in FCS and IDA countries to 30–33 percent of its guarantee volume by FY23.1 Both IFC’s and MIGA’s commitments may lead to significant increases in business in FCS, but at present, the institutions do not have an FCS-specific metric to measure their commitment to scale up investment and guarantee support under the Bank Group FCV strategy.

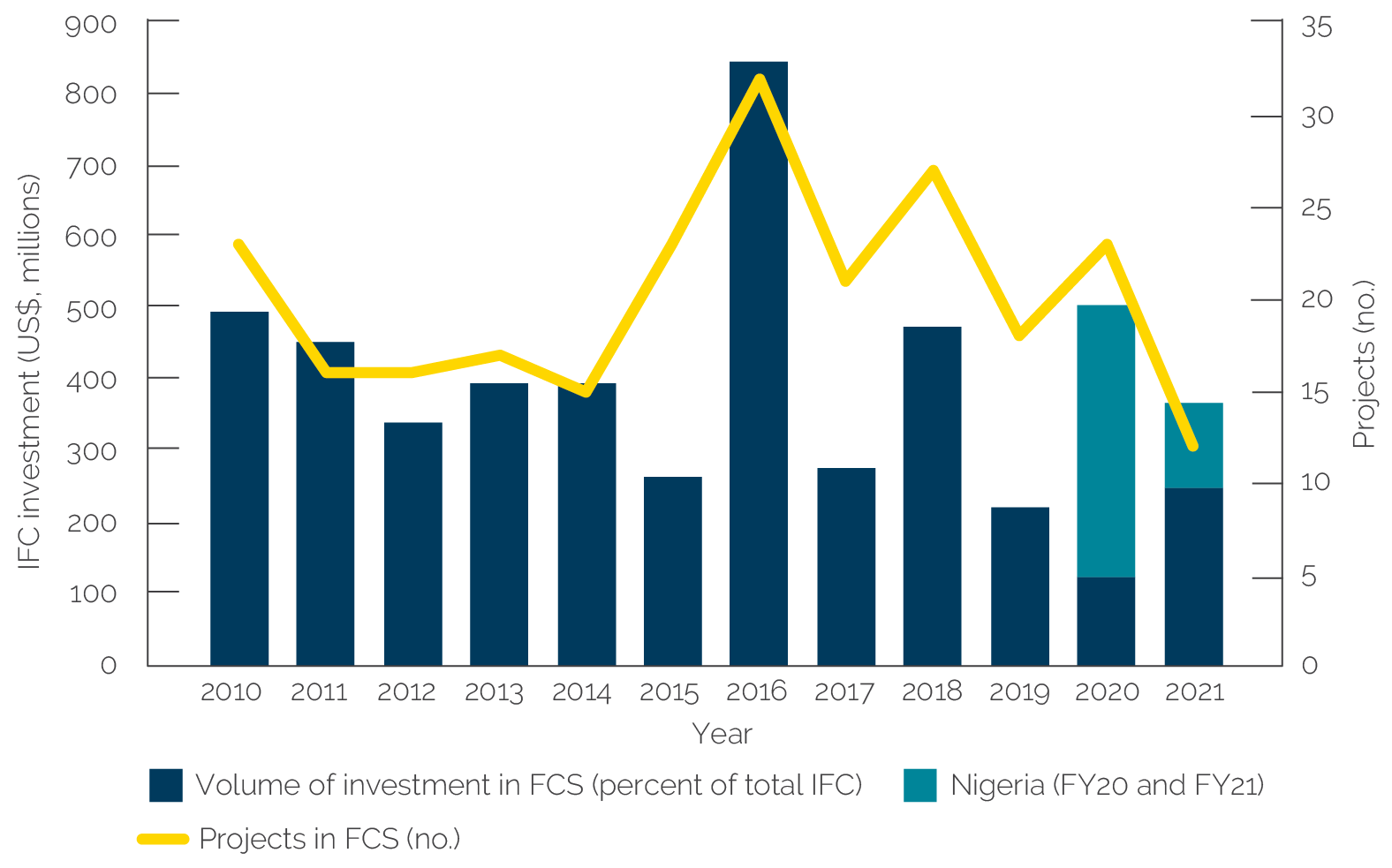

IFC’s business volume in FCS has been relatively flat since FY10, and scaling up has remained a challenge. From FY10 to FY21, long-term investments in FCS for IFC’s own account on average reached 5.2 percent of IFC’s total long-term commitments and 8.6 percent of the number of projects (figure 2.1).2 IFC’s annual commitment volumes in FCS averaged $420 million (FY10–21) with some volatility, which partly reflects the changing FCS country classification. For example, a strong increase in FY20 business volume is due to Nigeria’s addition to the FCS list.

Sources: International Finance Corporation and Independent Evaluation Group staff calculations.

Note: FCS = fragile and conflict-affected situations; FY = fiscal year; IFC = International Finance Corporation.

IEG has analyzed IFC’s commitments and MIGA’s guarantees based on the Harmonized List of Fragile Situations, given the methodological rigor and wide application of this classification. This list is produced by the World Bank and has been replaced since FY20 by a List of Fragile and Conflict-Affected Situations, which was developed as part of the FCV strategy. These numbers differ from those reported by IFC and MIGA for their engagement in FCS because of IFC’s convention to use a modified FCS definition and country list extending the FCS classification of countries by three years (para. 1.12).3, 4 Additionally, there are methodological challenges in classifying (and accounting for) IFC regional and global programs as FCS. The availability of data and method to determine FCS allocations for regional and global projects has evolved over time. Between FY16 and FY21, these projects provided an additional $479 million in commitments (based on the Bank Group’s harmonized list) to FCS countries. Appendix G provides further detail on definitional and methodological issues.

IFC’s commitments and MIGA’s guarantee volume in FCS countries are concentrated in a few countries that already attract relatively high levels of FDI, including resource-rich countries. The top six FDI-receiving FCS countries (Democratic Republic of Congo,, Lebanon, Nigeria, Mozambique, Myanmar, and the Republic of Congo) out of 37 FCS countries in FY20, account for three-quarters of FDI inflows to FCS (and 54 percent of IFC’s business volume and 60 percent of MIGA guarantee exposure in FCS). As shown in table 2.1, resource-rich FCS economies received 48.1 percent of IFC investments and 27.6 percent of MIGA guarantees in all FCS countries during the review period (FY10–21). By contrast, IFC and MIGA have yet to support investments in several of the FCS countries, including several of the small island developing states.

Table 2.1. FCS Share of FDI, IFC Own Account, Long-Term Investments, and MIGA Guarantees in Different Country Typologies (percent)

|

Country Typology |

Share of FDI, 2010–19 |

IFC Investments, FY10–21 |

MIGA Guarantees, FY10-21 |

|

All FCS countries |

100 |

100 |

100 |

|

IDA FCS |

88.0 |

72.0 |

92.7 |

|

Non-IDA FCS |

12.0 |

28.0 |

7.3 |

|

Resource-rich FCS |

48.3 |

48.1 |

27.6 |

|

Landlocked FCS |

10.9 |

7.4 |

8.5 |

|

Small island FCS |

2.5 |

8.3 |

0.4 |

|

Core (or always) FCS |

43.6 |

53.1 |

71.2 |

|

Transitional FCS |

40.5 |

46.8 |

28.8 |

|

Conflict FCS |

35.8 |

36.9 |

11.5 |

|

Fragility FCS |

52.9 |

36.1 |

36.3 |

Source: International Finance Corporation, Multilateral Investment Guarantee Agency, and Independent Evaluation Group staff calculations.

Note: Several typologies overlap, and totals exceed 100 percent. FCS = fragile and conflict-affected situations; FDI = foreign direct investment; FY = fiscal year; IDA = International Development Association; IFC = International Finance Corporation; MIGA = Multilateral Investment Guarantee Agency.

Short-term finance has been another mode of IFC engagement in FCS. Short-term financing increased significantly in FY20 as part of IFC’s COVID-19 response and reflects IFC’s extensive use of the existing platforms or programs (including with funds from the PSW).

Beyond commitments on its own account, IFC has mobilized more than $6.6 billion in private capital during FY10–21 in FCS. A significant share of mobilization was for infrastructure projects ($5 billion). One project alone accounted for almost half of the mobilization, the Nacala Corridor infrastructure project in Mozambique committed in FY18. A further $836 million was mobilized for public-private partnerships, and $525 million in the Financial Institutions Group. Over the entire period, the share of mobilized capital in FCS was 7 percent of IFC’s total mobilization.

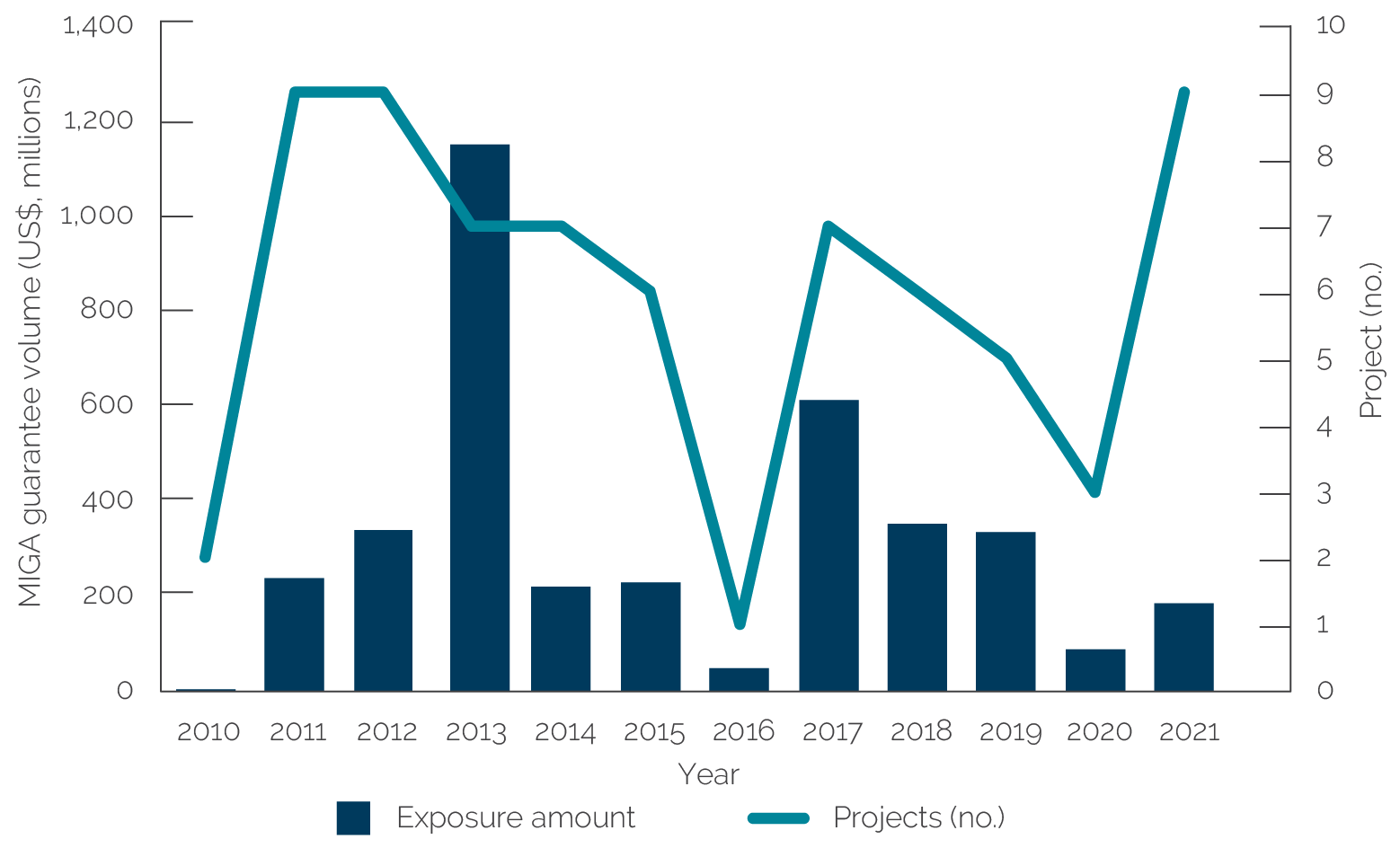

MIGA’s guarantee volume has not shown an upward trend (figure 2.2). During FY10–21, an average of 9 percent of MIGA’s new guarantee volume, or 17 percent of projects, was in FCS. Annual gross exposure averaged $317 million, with two outlier years (2013 and 2017) because of large infrastructure projects in Angola, Côte d’Ivoire, and Myanmar. MIGA’s support to FCS did not have an upward trend, despite the introduction in 2013 of MIGA’s Conflict-Affected and Fragile Economies Facility (CAFEF),5 providing a first loss guarantee that aimed to catalyze private capital flows from investors and financial institutions to FCS by mobilizing noncommercial risk insurance from MIGA and the global insurance industry. By type of risk coverage, insurance against war and civil disturbance represented 75 percent of all MIGA PRI in FCS and was often combined with coverage against transfer restriction and expropriation.

Source: Multilateral Investment Guarantee Agency and Independent Evaluation Group staff calculations.

Note: FCS = fragile and conflict-affected situations; FY = fiscal year; MIGA = Multilateral Investment Guarantee Agency.

In addition to its guarantee issuance, MIGA’s direct mobilization of private capital totaled $3.78 billion in FCS countries in FY10–21.6 Over the period, the share of directly mobilized capital in FCS countries represented 9 percent of total private direct mobilization reported by MIGA.

Sector Focus of IFC and MIGA-Supported Investments in FCS

IFC’s investment volume in FCS is driven by a limited number of infrastructure projects. Half of IFC’s long-term finance commitments support infrastructure projects, double the share in non-FCS countries (table 2.2). This reflects the financing needs in this capital-intensive sector, but it may indicate challenges in finding suitable investments and sponsors in other sectors. By number of projects, the Financial Institutions Group dominates, with 39 percent of all projects. This reflects the prevalence of larger-size infrastructure projects compared with the relatively smaller size of investments in the Financial Institutions Group and in manufacturing, agribusiness, and services, including support for microfinance institutions and leasing projects.

Table 2.2. IFC Long-Term Investments in FCS and Non-FCS, by Sector (FY10–21)

|

IFC Industry Group |

FCS (US$, millions) |

Share in FCS (%) |

Non-FCS (US$, millions) |

Share in Non-FCS (%) |

|

Infrastructure |

2,501 |

50 |

24,772 |

23 |

|

Financial Institutions Group |

1,382 |

27 |

45,451 |

43 |

|

Manufacturing, Agribusiness, and Services |

1,107 |

22 |

30,387 |

28 |

|

Disruptive Technologies and Funds |

56 |

1 |

6,184 |

6 |

Sources: International Finance Corporation and Independent Evaluation Group staff calculations.

Note: FCS = fragile and conflict-affected situations; FY = fiscal year; IFC = International Finance Corporation.

MIGA’s FCS portfolio differs from its non-FCS portfolio (table 2.3). Like IFC, the infrastructure sector dominates MIGA’s business volume in FCS (73 percent), whereas a small portion of gross exposure supports guarantees in the financial sector (16 percent)—the most important sector by volume in non-FCS countries. However, by number of projects, almost half of the MIGA-supported projects in FCS are in manufacturing, agribusiness, and services (44 percent). MIGA’s average gross exposure in FCS is less than half that in non-FCS ($32 million versus $84 million).

Compared with IFC investment activity, IFC advisory services for private firms and governments are concentrated more highly in FCS. FCS countries account for 16 percent of overall IFC advisory projects. In addition to advisory services to private firms, IFC—often in collaboration with the World Bank—has also supported business-enabling activities with governments aimed at addressing barriers to private sector growth and removing impediments to FDI. About 53 percent of IFC advisory services projects overall are directed to private firms, but this ratio is 49 percent in FCS countries.

Table 2.3. MIGA Guarantees in FCS and Non-FCS, by Sector (FY10–21)

|

Sector |

FCS (US$, millions) |

Share in FCS (%) |

Non-FCS (US$, millions) |

Share in Non-FCS (%) |

|

Infrastructure and energy |

2,764 |

73 |

18,160 |

45 |

|

Manufacturing, agribusiness, and services |

449 |

12 |

3,151 |

8 |

|

Financial |

591 |

16 |

18,375 |

47 |

Sources: MIGA and Independent Evaluation Group staff calculations.

Note: Infrastructure and energy includes the mining, oil, and gas sectors. Percentage columns may not total to 100 owing to rounding error. FCS = fragile and conflict-affected situations; FY = fiscal year; MIGA = Multilateral Investment Guarantee Agency.

Tailored Instruments and Initiatives

Over the evaluation period, IFC has deployed modalities and instruments, including some designed specifically for FCS countries. Under the IFC 3.0 strategy (IFC 2017), IFC has deployed diagnostic tools to support its engagement in FCS, including Country Private Sector Diagnostics, IFC country strategies, and the Anticipated Impact Measurement and Monitoring framework. It has implemented new approaches, such as Creating Markets (which promotes sector reform, standardization, building capacity, and demonstration to expand investment opportunities in key sectors); de-risking (PSW, guarantees, and blended finance resources); and upstream support (IFC 2016a). The FCV strategy (World Bank 2020b) flagged several adjustments in IFC’s approach to FCS, including (i) a differentiated approach aiming to tailor investment and advisory services to the different needs and capacities of each type of FCS; (ii) increased upstream engagement; (iii) enhanced inclusion and conflict sensitivity; (iv) a portfolio approach; (v) enhanced Bank Group collaboration; (vi) enhanced risk mitigation, in particular through blended finance solutions, including IDA PSW; (vii) streamlined programmatic approaches; (viii) greater collaboration with other DFIs; and (ix) strengthened staff presence and incentives. It is, however, too early to assess the impact of many of these recent initiatives.

IFC and the World Bank sought to support private investment indirectly by helping improve the business, legal, and regulatory environment through advisory services to governments. IFC also launched in 2008 the CASA initiative, a trust-funded program focused on FCS in Africa to help Africa’s FCS rebuild their private sectors, create jobs, and attract investment. More recently, IFC added the Creating Markets Advisory Window as a funding source for advisory work in IDA and FCS countries.

MIGA has mainly deployed one product in FCS countries—PRI—while using its nonhonoring insurance product once.7 MIGA’s political risk instrument offers guarantees against certain noncommercial risks, such as war and civil disturbance, expropriation, and transfer restrictions. The minimal use of the nonhonoring insurance is due to MIGA’s sovereign credit risk requirement (BB−) for that product.8 In addition, MIGA has not deployed one of its PRI programs since FY17, the Small Investment Program (SIP), which is intended to provide streamlined, fixed pricing support to small and less-complex investments, especially in IDA, FCS, and South-South investments.9 SIP projects account for approximately 20 percent of MIGA’s portfolio in FCS (13 of the 62 FCS projects in FY10–20).

However, MIGA has adapted its instrument mix in FCS through several initiatives. It created the multicountry CAFEF in 2013 with the capacity to increase its guarantee volume in FCS by $500 million. The PSW also supports MIGA’s engagement in FCS, especially under its $500 million MIGA Guarantee Facility. In addition, the existing West Bank and Gaza Investment Guarantee Fund exceptionally allows coverage for local investment10 that has met demand, indicating its usefulness as a product extension in an FCS context. Coverage of local investment is generally not permissible under MIGA’s Convention because of the need to rely on bilateral investment treaties as a risk mitigation tool. However, MIGA’s experience under the West Bank and Gaza Investment Guarantee Fund offers lessons about the benefit of providing coverage to credible local investors that can drive foreign investments in FCS.11

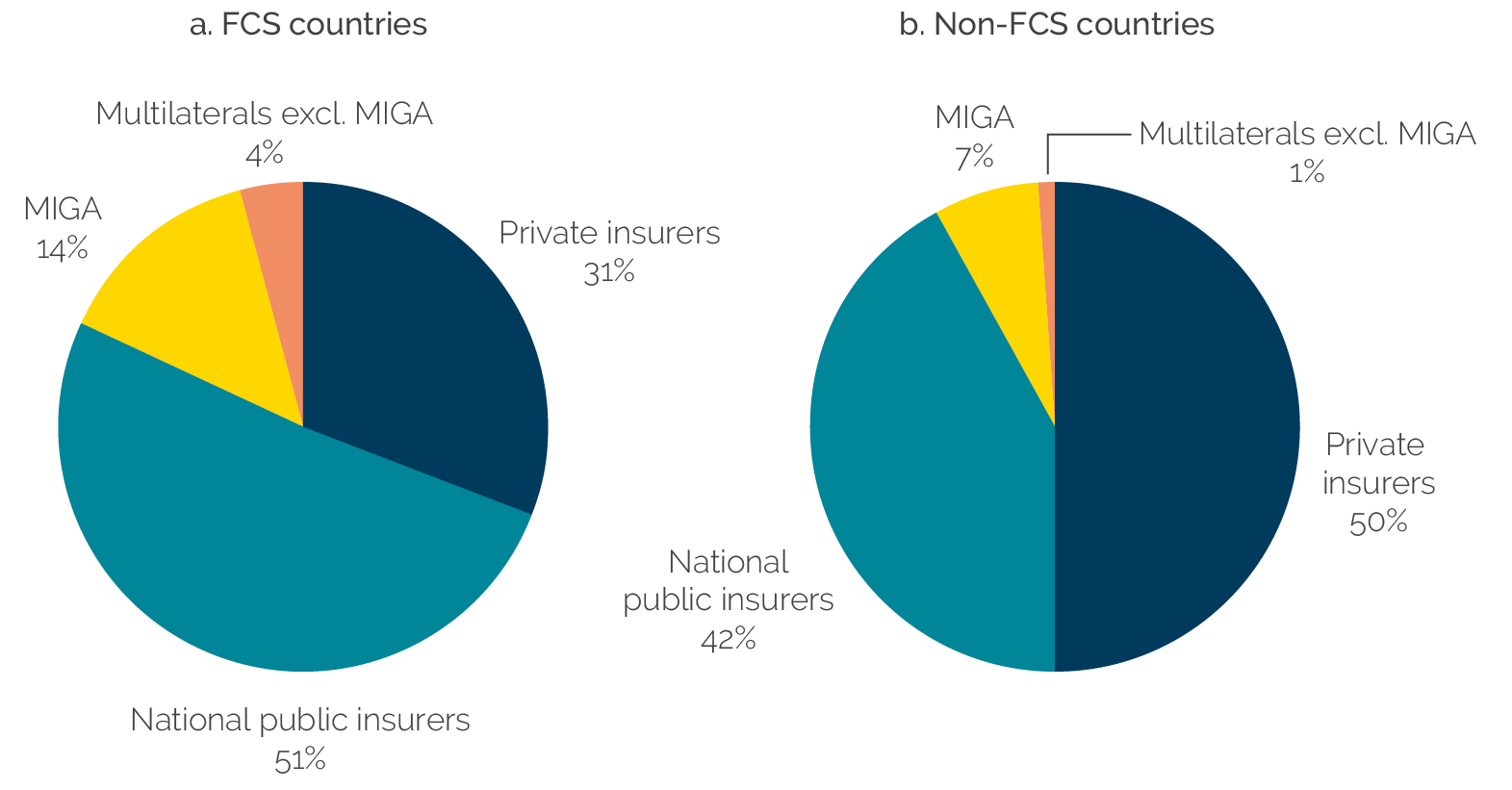

MIGA’s share of new investment insurance business in FCS is higher compared with other multilateral insurers. During the past 10 calendar years (2010–20), MIGA’s average share of new PRI issued to support investments in FCS (14 percent)12 exceeded that of other multilateral members (4 percent) of the Berne Union. MIGA’s share of the PRI market is also greater in FCS than in non-FCS countries, indicating MIGA’s comparative advantage in risky markets and a potentially more important role for MIGA in FCS markets than non-FCS markets (figure 2.3). However, private and national public investment insurers still account for the substantial share of investment insurance offered in FCS countries.

Figure 2.3. MIGA’s Share of New Political Risk Insurance in FCS and Non-FCS (2010–20)

Figure 2.3. MIGA’s Share of New Political Risk Insurance in FCS and Non-FCS (2010–20)

Source: Berne Union Investment Insurance database and Independent Evaluation Group calculations.

Note: (i) The above charts exclude new political risk insurance issued by Sinosure (China’s national export credit and export insurance agency), whose share averaged 64 percent of new business issued by Berne Union members in calendar years 2010–20. (ii) Berne Union data are reported by calendar year. FCS = fragile and conflict-affected situations; MIGA = Multilateral Investment Guarantee Agency.

IFC and MIGA deploy blended finance instruments that can help develop the private sector by mitigating financial risks. Blended finance facilities deployed in FCS include the Global Agriculture and Food Security Program, the Global SME Finance Facility, and climate and gender inclusion. The PSW is the Bank Group’s most recent and largest blended finance instrument to support private investments in IDA and FCS countries. The PSW’s objective is to mobilize private sector investments in underserviced sectors and markets in the poorest and most fragile IDA countries. It is designed to de-risk investments to make them more commercially viable or to limit IFC’s or MIGA’s own exposure to project risk.

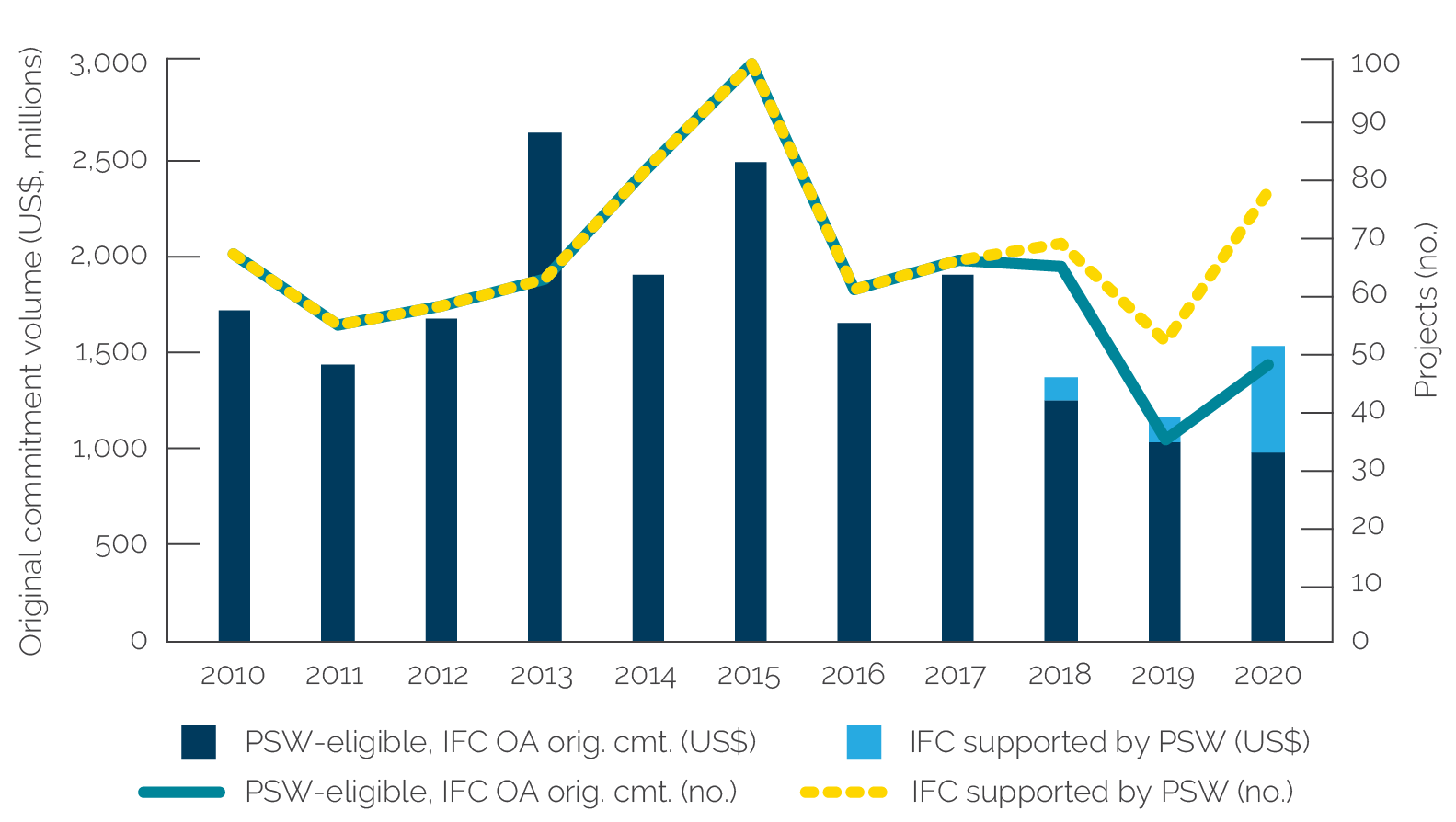

However, the PSW has not contributed to an increase of business volume in PSW-eligible countries during the 18th Replenishment of IDA (IDA18; figure 2.4). PSW participation showed some positive effects in allowing the institutions to enter new markets or sectors. But IFC commitments and MIGA guarantee volumes in eligible countries remained relatively stable during IDA18, and IFC’s and MIGA’s usage of the PSW has been well below the original IDA18-allocated amounts. Under IDA18, which spanned FY18–20, $1.37 billion in PSW funds were approved for investment, equal to 55 percent of IDA funds allocated ($2.5 billion) for the PSW. Most approvals occurred in the final quarter of FY20, coinciding with the Bank Group’s COVID-19 crisis response. Contributing factors included strict eligibility criteria, limited pipeline, longer gestation period for projects, and the start-up of PSW in IDA18 (World Bank 2021b). Regarding the concessionality13 of the PSW, a robust process determines the subsidies needed to make IFC and MIGA projects more commercially viable, emphasizing minimum concessionality.

Figure 2.4. IFC Commitment Volumes and Number of Projects in PSW-Eligible Countries for Long-Term and Short-Term Finance, Own Account, FY2010–20

Figure 2.4. IFC Commitment Volumes and Number of Projects in PSW-Eligible Countries for Long-Term and Short-Term Finance, Own Account, FY2010–20

Sources: International Finance Corporation and Independent Evaluation Group staff calculations.

Note: The commitment and project data exclude regional projects that may benefit PSW-eligible countries partially. Cmt. = commitment; FY = fiscal year; IFC = International Finance Corporation; OA = own account; orig. = original; PSW = Private Sector Window.

Achievement of Development Outcomes in FCS

Project Outcomes

IEG assessed development outcomes using outcome ratings of evaluated IFC and MIGA projects and findings from case studies. Development outcome ratings for IFC and MIGA projects are synthesis ratings assessing the project performance in four dimensions: business success, contribution to economic sustainability, E&S effects, and private sector development impacts.

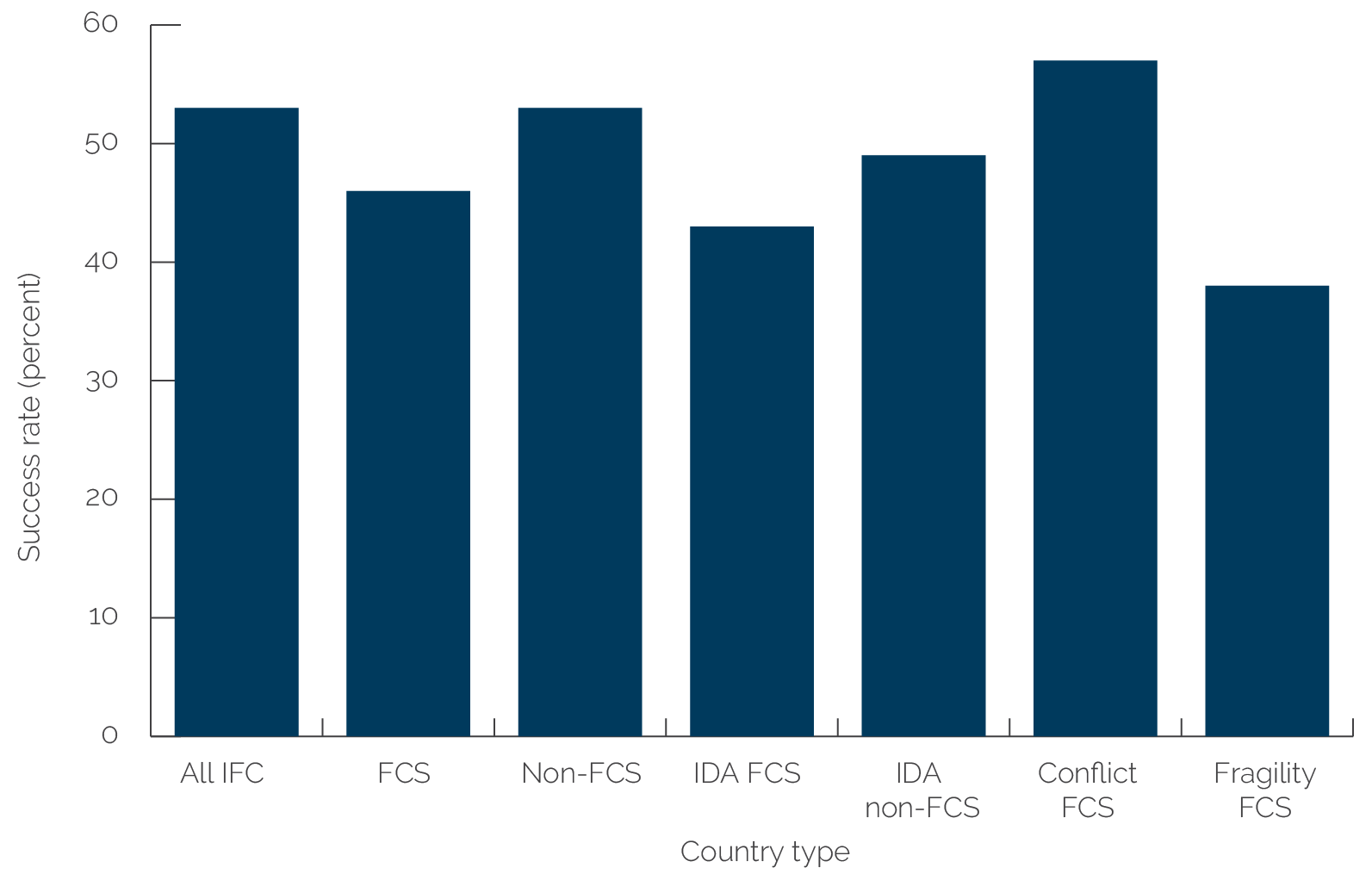

IFC’s development outcome ratings in FCS have been like those in non-FCS countries. Forty-six percent of projects in FCS have positive outcome ratings, compared with 53 percent in the rest of the portfolio. This is based on 59 evaluated IFC FCS projects and 817 non-FCS projects (figure 2.5).

Figure 2.5. IFC Development Outcomes, 2010–2020

Figure 2.5. IFC Development Outcomes, 2010–2020

Source: Independent Evaluation Group staff calculations.

Note: FCS = fragile and conflict-affected situations; IDA = International Development Association; IFC = International Finance Corporation.

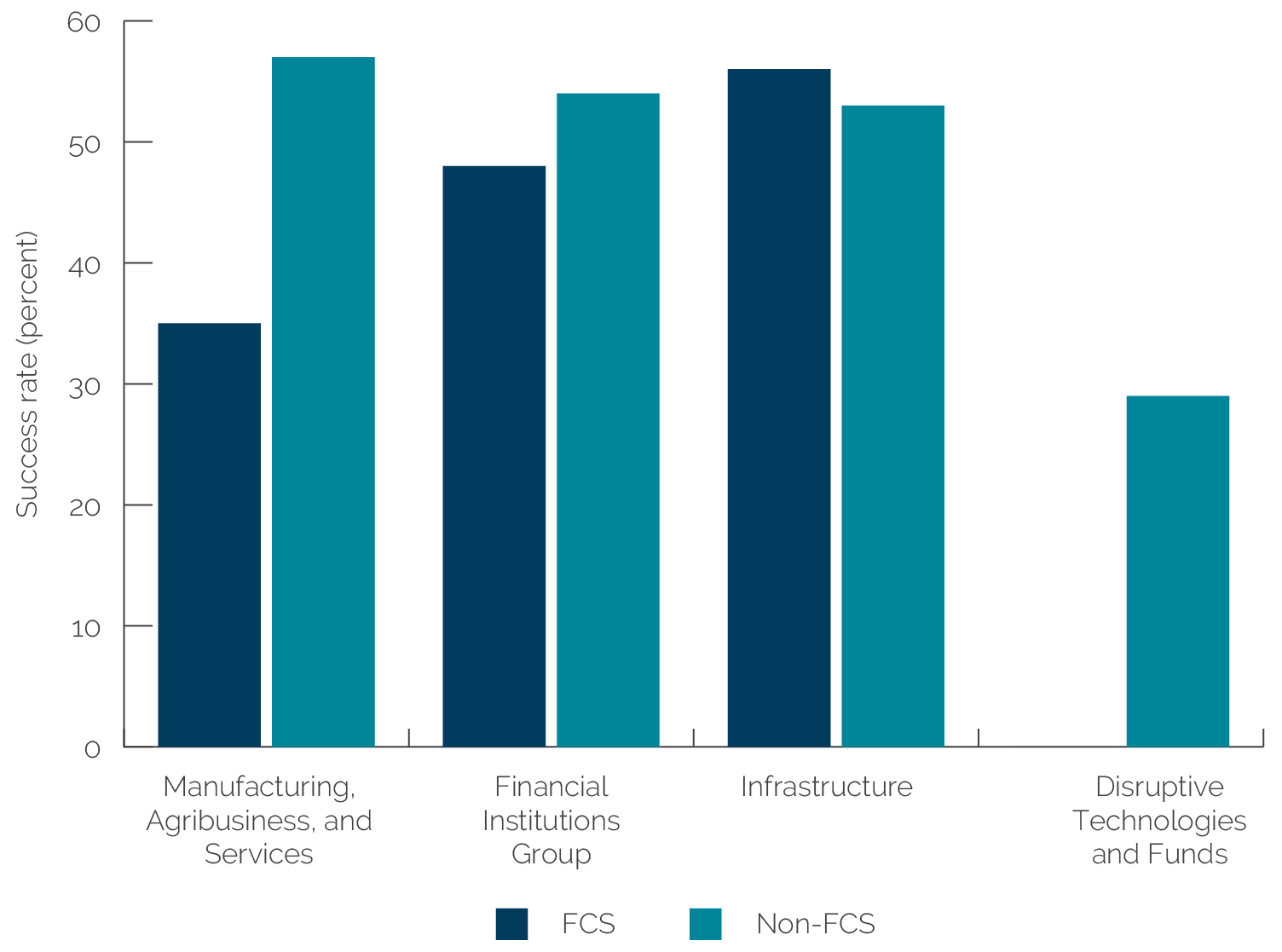

Determinants of the performance of IFC projects in FCS include the nature of the sector, the investment size, the size of the economy, quality of clients, client characteristics (new or repeat), and the quality of IFC’s assessment. Infrastructure projects in FCS performed well (56 percent; figure 2.6), often using internationally experienced project sponsors or project developers. By contrast, only 35 percent of the evaluated Manufacturing, Agribusiness, and Services projects in FCS were rated as mostly successful or higher, driven mostly by low ratings in agribusiness and the group’s other subsectors, whereas manufacturing projects in FCS performed relatively strongly. Financial Institutions Group projects performed similarly in FCS and non-FCS countries, despite differences in the composition of the group’s portfolios, such as the prevalence of smaller, less-sophisticated financial institutions (microfinance institutions and leasing companies) in FCS.

Source: Independent Evaluation Group staff calculations.

Note: FCS = fragile and conflict-affected situations; IFC = International Finance Corporation.

The size of the country and the investment are correlated with performance. Evaluated projects in larger FCS countries (by size of the population) performed better than those in midsize countries (60 percent versus 35 percent) or small economies (35 percent). A similar pattern emerges for the size of IFC commitment. Relatively large IFC investments (more than $35 million in commitments) perform well (67 percent) compared with medium and small investments (46 percent and 36 percent, respectively).

The performance of projects in FCS involving repeat clients is stronger than one-off projects. Thirty-nine percent of IFC’s projects in FCS are with repeat clients. As is the case for IFC projects overall, repeat projects perform significantly better than those with one-off clients (84 percent versus 29 percent), contributing to IFC’s results in FCS. For example, the ACLEDA Bank project in Myanmar built on earlier IFC investments in Cambodia and the Lao People’s Democratic Republic. IFC’s engagement with the ACLEDA Group began in 2000 with an equity investment in ACLEDA Cambodia, where IFC helped ACLEDA build its operational base and grow into the largest financial institution. IFC then supported ACLEDA’s regional expansion into the Lao People’s Democratic Republic in 2008 and Myanmar in 2013, where it is now the sixth largest microfinance institution. However, the SolTuna Capex project in the Solomon Islands was IFC’s first engagement with the sponsor, one of the world’s largest tuna suppliers. Although extensive IFC advisory services on E&S and gender supported the project (along with complementary World Bank policy initiatives), a change in ownership led to the loan being prepaid due to the new owner’s access to cheaper financial resources.

Despite this development outcome performance, a key challenge for IFC in FCS contexts remains ensuring additionality,14 particularly in follow-on projects with well-established sponsors. For example, in the Gulftainer II project (involving the development, construction, and operation of an inland container depot and logistics center in Iraq), IFC‘s stated expected additionality comprised provision of a long-term loan (up to 11 years) that was not available from commercial banks, as well as IFC’s ability to influence the client to undertake measures to comply fully with E&S standards. However, IEG’s evaluation noted that the company prepaid its loan in 2 years. In addition, the project already complied with IFC E&S standards. IFC’s investment also had a corporate guarantee from the United Arab Emirates–based company, removing Iraq country risk, and included an upside “sweetener.” In these circumstances, alternative commercial finance would likely have been available for the project. Notwithstanding the project’s location in an FCS, IFC’s low additionality suggests that the investment and development benefits would have occurred even without IFC’s investment.

The development effectiveness of IFC advisory services is rated lower in FCS countries than in non-FCS countries. FCS advisory services projects were rated successful in 47 percent of cases compared with 56 percent of non-FCS advisory services projects. FCS projects were also rated somewhat lower for their strategic relevance.

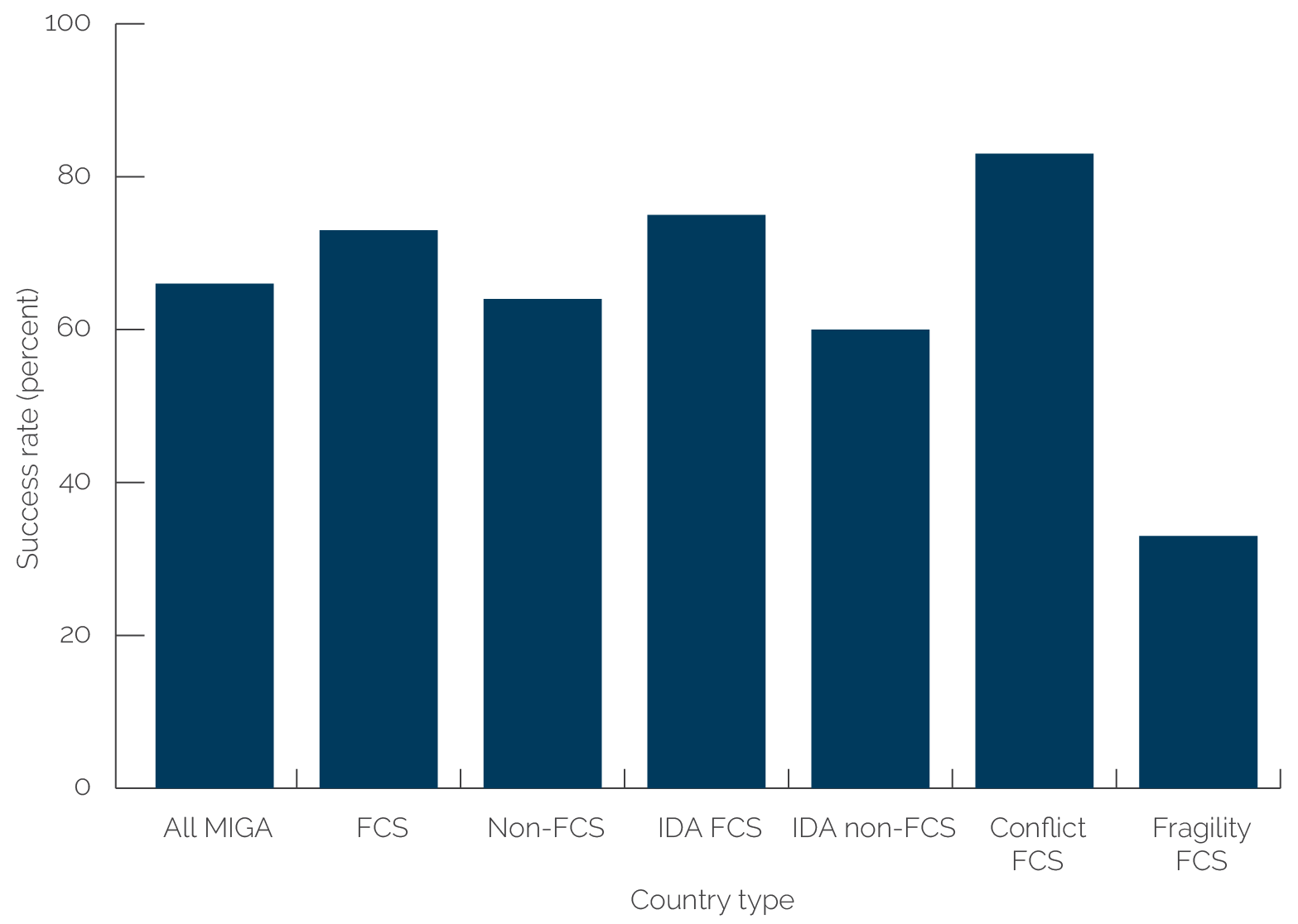

Evaluated MIGA projects in FCS countries performed better than in non-FCS countries. Seventy-three percent (16 of 22) of evaluated FCS projects were rated satisfactory or better for their development outcome, which measures the project’s business performance, economic sustainability, E&S effects, and contribution to private sector development.15 By contrast, 64 percent (72 of 112) of evaluated projects in non-FCS countries (figure 2.7) were rated satisfactory or better in achieving their development outcomes. Although the small number of evaluated projects in FCS precludes cross-country or cross-sector inferences (table 2.4), this set of projects outperformed evaluated projects in non-FCS countries in three of the four development outcome subindicators, namely business performance, economic sustainability, and contribution to private sector development. Evaluated projects in non-FCS countries outperformed projects in FCS in their E&S effects: 75 percent of evaluated projects in non-FCS were rated satisfactory or better compared with 65 percent (11 of the 17 projects with E&S effects rating). Evaluations of MIGA projects indicate that the project sponsor’s experience, technical expertise, financial capacity, and knowledge of local conditions are critical factors in operating successfully in FCS, as these traits have ramifications for project design and operation in risky and uncertain environments. The need for proper assessment and monitoring by MIGA of conflict and fragility risks in addition to sector risks are also lessons gleaned from the evaluated projects.

Source: Independent Evaluation Group staff calculations.

Note: FCS = fragile and conflict-affected situations; IDA = International Development Association; MIGA = Multilateral Investment Guarantee Agency.

Source: Independent Evaluation Group staff calculations.

Note: FCS = fragile and conflict-affected situations; FY = fiscal year; IDA = International Development Association; MIGA = Multilateral Investment Guarantee Agency.

However, the MIGA FCS projects that are supported by the SIP are not evaluated by IEG or MIGA, although this instrument is deemed highly relevant to MIGA’s engagement in FCS. MIGA’s project evaluation program does not systematically cover SIP-supported projects, although they made up approximately 20 percent of MIGA’s guarantee projects in FCS (13 of the 62 FCS projects in FY10–20). The lack of evidence about the SIP projects’ outcomes creates a knowledge gap and limits the potential for learning from this set of projects in FCS. Evidence from one evaluated project indicated the feasibility of covering SIPs through MIGA’s evaluation program, yielding useful lessons. Learning from recent SIP experience can help inform MIGA’s plan to streamline and potentially scale up the program as part of its business model in IDA FCS countries, which is outlined in the Bank Group FCV strategy.16

MIGA relied on repeat clients for its business in FCS, and those projects performed well. More than half of MIGA’s FCS projects involve repeat clients, and their success rate is 70 percent. For example, MIGA supported a series of logistics projects providing border inspection equipment in several African countries, most of which performed well. Appendix C provides outcome ratings for IFC and MIGA projects.

The high outcome ratings also reflect MIGA’s focus on working with strong sponsors. Strong performance was associated with sophisticated international companies and guarantee holders with experience in implementing projects in developing markets. Unlike IFC, which can also work with some smaller, local investors, MIGA insures foreign companies’ cross-border investments. Foreign investors tend to be better capitalized and have larger asset bases and diversified revenue sources compared with local firms.

Among the case studies conducted for the evaluation, three-fourths of IFC and MIGA projects studied in depth experienced conflict- or fragility-related FCS risks, three-fourths experienced challenges related to government capacity, and all four financial intermediary projects faced weak or underdeveloped policy and enabling environments. FCS risks and constraints were rated significant or high in six cases, such as political violence against a religious minority state in Myanmar and severe political instability that occurred during the project life cycle in the Democratic Republic of Congo. The project team in the Democratic Republic of Congo highlighted multiple development challenges, ranging from weak institutions and poor governance to persistent violent conflict among militias and with government forces (particularly in the eastern regions) to a growing youth bulge without adequate access to job opportunities. A venture fund had intended to make investments in both the Democratic Republic of Congo and the Central African Republic, but when a full civil war broke out in the Central African Republic soon after the fund’s inception, the fund focused its activities on the Democratic Republic of Congo.

Most projects experienced challenges related to government capacity. Inadequate government capacity and governance risks were significant in four projects and moderate in another five. For projects with a significant or high rating, instances involving government capacity and governance issues had a bigger impact or were more difficult to mitigate. The Rawbank project in the Democratic Republic of Congo struggled because of a lack of regulatory and financial infrastructure to facilitate access to credit in the Democratic Republic of Congo, which also lacked a properly functioning commercial legal system to resolve disputes for small and medium enterprises (SMEs) and effective collateral and credit information systems for SMEs. In Myanmar, a change in administration after the 2015 election led to difficulties in acquiring government approval for several key project documents for an independent power producer (IPP) project, resulting in significant project delays. Other than this competitively tendered project, the government’s preference in the power and other infrastructure sectors was the country’s traditional practice of using direct negotiations and unsolicited proposals.

Achievement of Environmental, Social, and Gender Objectives

Environmental, social, and gender objectives are important aspects of IFC’s and MIGA’s value addition with their clients, due to weak public and private capacity in FCS and their link to make private investments more sustainable and inclusive. The E&S performance for evaluated projects was weaker in FCS countries than in non-FCS countries. Fifty-five percent of IFC projects in FCS were rated mainly satisfactory or above versus 69 percent in non-FCS. For MIGA, two-thirds of evaluated FCS projects were rated satisfactory (versus 75 percent in non-FCS).

The E&S issues encountered in FCS countries are largely like those in low-income, non-FCS countries. For example, in the Solomon Islands, the Tina River Hydropower Development Project is located on forest and agricultural lands customarily owned by five local tribes. Although no households were displaced, the land was procured under a land lease agreement with a joint venture between the landowning tribes and the government, with payments going into a unique benefit-sharing mechanism to benefit the wider community. The Azito III project in Côte d’Ivoire established a similar local development fund to compensate villagers for the government’s inability to find suitable replacement land to resolve legacy claims dating from the project’s first phase more than a decade earlier. Two of the financial sector projects in the sample—Rawbank in Democratic Republic of Congo and Société Ivoirienne de Banques/Cargill in Côte d’Ivoire—faced the same types of E&S compliance monitoring and reporting issues that financial inter-mediary projects in non-FCS countries encounter frequently.

Regarding the E&S effects, all projects in the evaluation sample rated E&S factors as having negligible or moderate effects except for three projects, for which no opinion was possible. However, projects with a moderate rating noted challenges that were difficult to address. For example, the Myingyan IPP project (a 225-megawatt gas-fired power plant in Myanmar) faced scrutiny from local and international nongovernmental organizations on the transparency of the power purchase agreement’s terms and on E&S matters, which the lender’s E&S specialists considered to be technically unfounded. Despite this, the lenders recommended that the client take concrete measures to improve stakeholder communications and build mutual trust with local communities to mitigate the concerns.

IFC and MIGA apply the same E&S performance standards in FCS countries as in non-FCS countries. Considering the more challenging operating conditions in FCS, the Bank Group has usually taken the lead in supporting E&S-related policy reforms and institutional capacity strengthening. IFC takes the lead where IFC and MIGA have a joint project. IFC and MIGA have also adapted the intensity of monitoring and supervision to the client’s E&S risk review rating. The evaluation found little information on projects that were deemed ineligible for support because of E&S issues or risk.

The main factor affecting E&S performance is sponsor commitment and capacity, so IFC and MIGA must assess that factor and any capacity gaps carefully as part of their client selection process. For example, in the agribusiness sector, IFC is looking for committed clients to work on supply chain E&S issues that in the past had tended to rely on sustainability certification (by the UTZ certification program, the Rainforest Alliance, and so on). More recently, the integrity of certification has been compromised. The certifications have lost credibility and reached saturation from the consumer demand side. IFC now tends to help clients strengthen their own internal standards, sourcing controls, and surveillance systems, coupled with independent verification. In Côte d’Ivoire, it pursued such approaches with Cargill and other clients (Olam International and Barry Callebaut).

The effectiveness in mitigating E&S risks with IFC projects in FCS has been mixed. Some projects have experienced significant improvements in client E&S management system capacity (for example, AUB Iraq, Nafith Iraq, Rawbank DRC, SolTuna, and the Tina River Hydropower Development Project, with the latter two in the Solomon Islands), but projects encountered challenges with legacy land acquisition issues (Azito) and in monitoring and reporting (Cargill in Côte d’Ivoire and Myingyan in Myanmar).

IFC’s focus on gender issues in FCS is reflected in various corporate policies and strategy documents. Gender is emphasized as a key strategic cross-cutting priority under IFC 3.0 and in the World Bank Group’s FCV strategy. During FY10–20, the IFC portfolio included 14 gender-flagged projects in FCS countries, accounting for $328 million in commitments. Overall, even though the proportion of IFC’s gender-flagged projects and commitment volume in FCS remained relatively low, a broad spectrum of gender issues was addressed.

Expanded advisory services were instrumental in enabling IFC to engage a few of its FCS clients on gender issues. The Pacific WINvest Advisory Services Project (which IFC and the World Bank implemented jointly) directly supported IFC’s SolTuna project in the Solomon Islands to identify and implement gender-specific practices to improve conditions for their female employees to solve absenteeism that was affecting SolTuna’s financial results. By assessing and measuring conditions before and after the intervention, the program could track and document improvements over time. In Mali, the Mali Shi project (approved in 2019) is complemented by advisory services that offer training in business skills, finance, and management to members of 100 women-led cooperatives that work with Mali Shi. The project is expected to source shea nut kernels locally and thereby provide access to markets and improved income to about 120,000 shea collectors, about 95 percent of whom are women.

Achievement of Private Sector Development and Broader Development Outcomes

Implementing successful projects in FCS goes beyond the projects’ direct impact and the demonstration effects for future, similar projects. Overall, two-thirds of evaluated IFC projects in FCS achieved satisfactory ratings for their private sector development impact, which assesses the effects beyond the investment project. This rating is similar to that for the share of non-FCS projects. Seventy-seven percent of MIGA’s evaluated guarantees in FCS were rated satisfactory for their contribution to private sector development.17 Among the country and project cases reviewed in depth, most projects contributed to private sector development, including evidence of increased private investment beyond what IFC and MIGA facilitated, development of local markets, demonstration effects, and strengthening of corporate governance.

The review of evaluative evidence for IFC and MIGA projects indicates limited demonstration effects. In some sectors, the demonstration effect was limited, given the projects’ small size and insular nature relative to the country’s needs and because of the existence of few potential clients with whom IFC could work. This includes some banking operations that did not expand into underserviced client segments as anticipated. In the Democratic Republic of Congo, for example, because of poor critical infrastructure or a lack of any infrastructure, the domestic market was often limited to urban concentrations, and therefore the development impact of IFC’s and MIGA’s projects was limited to Kinshasa and a few other cities, with little or no penetration in other urban or rural communities.

The following examples illustrate effects beyond what the project intended, supporting private sector development and broader sector objectives, based on country and project case evidence in FCS:

- In the financial sector, IFC’s sustained investment and significant advisory program with a long-standing regional partner, ACLEDA, helped establish the first commercially oriented microfinance bank in Myanmar. The ACLEDA Myanmar Microfinance Institution (AMM) project saw commercial success and helped demonstrate good microfinance practices. As the first commercially oriented microfinance institution in Myanmar, AMM had a demonstration effect that encouraged other entrants and helped increase competition in the sector. Other lenders replicated the structure of AMM’s IFC loan. AMM also helped demonstrate good practices in microfinance, including in responsible finance and transitioning from basic group lending to more advanced individual credit lending. As of May 2020, AMM had an outstanding loan portfolio of more than $36 million and more than 100,000 outstanding loans, including loans for the agriculture sector, urban micro enterprises, and women. A parallel Bank Group support helped improve the regulatory environment for microfinance that improved the operating environment for microfinance institutions substantially after 2016. IFC also provided an industry-wide training program in the microfinance sector targeted at both regulators and micro finance institutions.

- Although earlier SME ventures funds had weak financial sustainability, the Central Africa SME Fund had some demonstration effects and involved learning. The fund manager was able to raise a larger follow-on fund targeting FCS countries (the African Rivers Fund). The original fund also helped build local capacity on how to run a private equity fund. IFC launched second-generation SME ventures funds that are larger and seek to learn from the earlier experience. The IDA PSW SME Ventures Envelope was approved in 2019 to co-invest up to $50 million from the PSW, with IFC expected to match that amount and other investors providing up to $400 million. IDA PSW SME Ventures Envelope was set up to make private equity funds in PSW-eligible countries less risky to investors, including IFC, by including PSW as a subordinated equity investor, generally with an investment equal to that of IFC. As of the end of FY21, IDA PSW SME Ventures Envelope has been committed to seven funds, of which three used the subordination feature. The program includes a set of IFC advisory services targeting both the regulatory environment and support for fund managers and target investees.

- In the power sector, the IFC- and MIGA-supported Myingyan power plant was linked to sector reform and was the first IPP in Myanmar to help raise Myanmar’s installed power generation capacity. The 225-megawatt gas-fired power plant in the Myingyan region was Myanmar’s first international IPP tender in the country and included a set of commercially bankable documents (including the power purchase agreement) that were developed with IFC assistance. The project’s development outcomes included increasing the country’s overall power generation capacity by 6.2 percent from 2013 levels and helping to meet the power needs of approximately 5.3 million people.

- In Myanmar, private participation in power generation increased substantially after the project, although its IPP framework was not replicated as expected. The project helped demonstrate that the country was open to private investment in the power sector. Between 2013 and 2018, FDI in the power sector amounted to $14.6 billion, equivalent to 25 percent of total FDI during the period. Projects included gas to power, hydropower, emergency gas, and solar power. The share of installed capacity of privately owned power plants rose from 27 percent in 2008–09 to 44 percent in 2019. However, the projects that followed did not use the international competitive tender model developed for the Myingyan IPP. The government instead tended to use unsolicited proposals and direct negotiation in developing projects, maybe because of a change in government or limited capacity, or because of concerns about “fiscal burden.” Neither IFC nor MIGA has engaged in power generation in Myanmar since the Myingyan project.

Overall, there are limited systematic data available to assess broader project impacts beyond development outcomes and no information available on the projects’ effects on resilience and conflict sensitivity. The review of sample projects found that job creation data, for example, are reported in less than half of the sample projects (5 of 12), only two sample projects report significant effects on gender equity, and two projects hint at some potential contribution to reduction of interethnic tensions.

Implications of Worsening Global Fragility and COVID-19

The increase in fragility and conflict during the past decade, exacerbated by COVID-19, have likely affected private sector activity and investment. The past decade has seen an increase in violent conflict, forced displacement, and subregional fragility and conflict (for example, in the Sahel, Lake Chad, and Horn of Africa regions). Several countries experienced reversals of progress (Afghanistan, Chad, Ethiopia, Mali, Mozambique, and Myanmar). The increase in fragility and conflict risks has likely constrained cross-border investments, and though the local private sector can be remarkably resilient during conflict, it may downscale or become more informal because of conflict and the collapse of government services (World Bank 2013).

COVID-19 has exacerbated these trends with likely knock-on effects on IFC’s and MIGA’s portfolio. FCS countries face numerous constraints that undermine their ability to cope with the COVID-19 crisis, including weak government capacity to manage the response, underdeveloped health systems, and poor infrastructure. The disruption in more developed countries also results in negative spillovers because both remittances and the supply chains needed to deliver humanitarian aid, food, vaccines, and curative drugs are affected. The combined economic and social shocks can also worsen fragility risks.

IFC identified impacts of the pandemic across different sectors—from tourism and hospitality to textile manufacturing and infrastructure—caused by disruptions to global trade and supply chains, travel, and tourism. The financial sector experienced an increase in nonperforming loans, and the limited availability of credit may force micro, small, and medium enterprises to cease operations. In response, the Bank Group launched the COVID-19 Crisis Response, which includes IFC’s $8 billion COVID-19 Fast-Track Facility to respond to the trade and short-term (working capital) liquidity needs and address the real sector impacts on existing clients (IFC 2020c). The latest data indicate that the macroeconomic effects of COVID-19 on FCS have been severe but also consistent with developing countries as a whole and varying significantly from country to country.18 Taken together, the disruptions and increase in uncertainty in FCS economies are likely to affect IFC’s and MIGA’s ability to scale up business and to reach financial and development benchmarks for projects in their existing portfolios.

- This commitment comingles volume growth in all International Development Association and fragile and conflict-affected situations (FCS) countries, with the target presented as an average of FCS and IDA17 (17th Replenishment of IDA) for fiscal year (FY)21–23.

- The shares of commitments and projects have been calculated excluding International Finance Corporation (IFC) global and regional projects from the numerator and denominator.

- For the Harmonized List of Fragile Situations, see appendix D, and for the Classification of Fragile and Conflict-Affected Situations, see https://www.worldbank.org/en/topic/fragility conflictviolence/brief/harmonized-list-of-fragile-situations.

- IFC’s reporting methodology was formalized in Guidance on Country Reporting (July 1, 2019).

- The Conflict-Affected and Fragile Economies Facility is a donor partner trust fund administered by the Multilateral Investment Guarantee Agency (MIGA) that provides a first loss layer for eligible cross-border investments in FCS countries, and MIGA shares a portion of the risk in the initial loss layer. Eligible coverages may include transfer/convertibility risk, expropriation, breach of contract, war and civil disturbance, nonhonoring of sovereign financial obligations, and any noncommercial risks approved by the MIGA Board pursuant to article 11(b) of the MIGA Convention and paragraph 1.53 of the Operational Regulations.

- MIGA mobilization numbers are based on the World Bank Group scorecard. From FY16 onward, estimations are based on the multilateral development banks’ Methodology for Private Mobilization. For the FY10–15 period, MIGA gross issuance is used as a proxy for private direct mobilization (while private indirect mobilization is not available).

- MIGA’s nonhonoring insurance product is insurance against nonhonoring of financial obligations by sovereign and subsovereign entities and state-owned enterprises. It provides protection against losses resulting from the failure of a sovereign entity, subsovereign entity (that is, city, municipality, or region), state-owned enterprise, and, more recently, regional development bank to make a payment when due under an unconditional and irrevocable financial payment obligation or guarantee related to a MIGA-insured investment. The nonhonoring product supports purely public sector undertakings or projects.

- MIGA may also have limited scope for deploying its nonhonoring insurance product to investments in FCS countries because of the limits imposed by International Monetary Fund–World Bank–Group of Twenty Debt Service Suspension Initiative on the countries experiencing high debt distress, most of which are FCS.

- The objectives of MIGA’s Small Investment Program when the program was presented to the MIGA Board in 2005 were to (i) increase MIGA’s direct support to small and medium enterprises; (ii) encourage small and medium investors; and (iii) help MIGA reach investors from nonindustrial countries (i.e., South-South investors) by offering fixed, subsidized pricing and reduced processing time through delegated Board approval of MIGA’s director of guarantee operations/senior management team.

- Under the trust fund, MIGA can provide political risk insurance to investments originating from any of its member countries and destined for the West Bank and Gaza. Local investments denominated in freely usable currency are also eligible. Eligible investors include companies or nationals of MIGA member countries; companies or nationals of members of multilateral organizations that are sponsors; or Palestinian residents or companies incorporated in the West Bank and Gaza. Source: West Bank and Gaza Investment Guarantee Fund Brochure.

- Conflict-Affected and Fragile Economies Facility, Donor’s Report H1 FY19, July 1, 2018, to December 31, 2018; and Conflict-Affected and Fragile Economies Facility Mid-Term Review (draft).

- This average share excludes the amounts issued by Sinosure (China’s national export credit and credit insurance agency), which dominated all other Berne Union members in new political risk insurance business in both FCS and non-FCS countries during the 10-calendar-year period 2010–20. Including Sinosure, the shares of private insurers, other national insurers, and multilateral insurers including MIGA shrinks considerably. As an example, MIGA’s average share is reduced to 5 percent from 14 percent; private insurers’ share of new business in FCS shrinks to 11 percent from 31 percent.

- Concessionality is based on the difference between (i) a reference price (which can be a market price, if available; the price is calculated using IFC’s pricing model, which comprises three main elements of risk, cost, and net profit, or a negotiated price with the client) and (ii) the concessional price being charged by the blended concessional finance co-investment. IFC calculates the level of concessionality as a percentage of total project cost: net present value of (reference price – concessional price)/total project cost = level of concessionality (expressed as a percentage of total project cost).

- Additionality is the unique support that IFC brings to a private investment project that is not typically offered by commercial sources of finance. Although related to an investment project, this additionality may take financial and/or nonfinancial forms. It is important to note that additionality is a threshold condition for IFC involvement in a project; it is not a policy or an objective, but rather a requirement embedded in IFC’s Articles of Agreement. IFC’s role, as a public institution supporting the private sector, is to provide services that are additional to those provided by private markets, while operating in a commercial manner. Indeed, article III, section 3 states that “the Corporation shall not undertake any financing for which in its opinion sufficient private capital could be obtained on reasonable terms” (https://www.ifc.org/wps/wcm/connect/corp_ext_content/ifc_external_corporate_site/about+ifc_new/ifc+governance/articles).

- The development outcome subindicator for contribution to private sector development was changed to foreign investment effects in June 2020.

- Refer also to Conflict-Affected and Fragile Economies Facility, Donor’s Report H1 FY20, July 1, 2019, to December 31, 2019, paragraph 17.

- MIGA project evaluations included an indicator assessing projects’ contribution to private sector development during most of the evaluation period; the indicator was changed in 2020 to capture foreign investment effects.

- According to the World Development Indicators database, remittances in FCS have declined from a high of $54.7 billion in 2019 to $46.7 billion in 2020. However, in the same year, both personal transfers and secondary income as a whole have increased slightly. The decline in gross domestic product, although more significant than in the world (5 percent for FCS versus 3.6 percent for the world), is driven by a few countries that have seen extreme declines (30 percent in Libya, 20 percent in Lebanon, and 10 percent in Iraq and Myanmar). With few exceptions, external debt has continued its increasing trend for FCS countries for which debt data are available.