IFC’s and MIGA’s Support for Private Investment in Fragile and Conflict-Affected Situations

Chapter 1 | Background and Approach

Highlights

The World Bank Group Strategy for Fragility, Conflict, and Violence 2020–2025 emphasizes the private sector’s importance for sustainable development in countries affected by fragility, conflict, and violence.

The International Finance Corporation and the Multilateral Investment Guarantee Agency have set ambitious targets for scaling up investments in fragile and conflict-affected situations.

This evaluation assesses how effective the two institutions have been in supporting private investment in fragile and conflict-affected situations, derives lessons from their experiences, and explores factors influencing the scale-up of their investments.

Background and Context

The private sector plays a critical role in providing jobs and income in countries affected by fragility, conflict, and violence (FCV).1 Although the private sector in fragile environments and in conflict situations is often informal, constrained, and distorted and may involve entities that are parties to conflict, it is acknowledged to have an essential role in providing livelihoods, income, and services2 to people. Inclusive and sustainable economic growth led by private investment can help heal grievances stemming from economic exclusion.

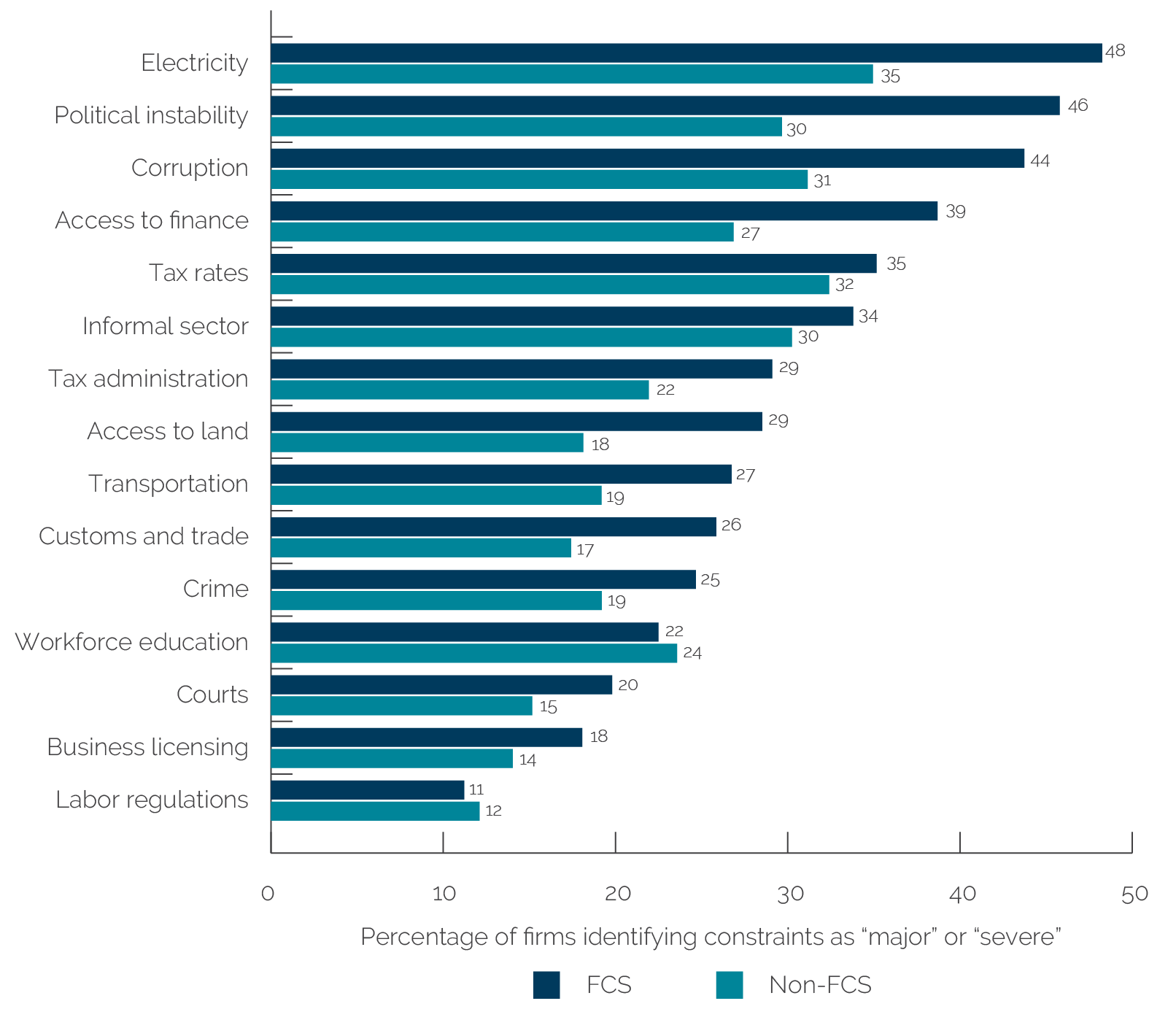

The World Bank Group Strategy for Fragility, Conflict, and Violence 2020–2025 emphasizes the importance of the private sector and private investment for sustainable development in FCV (World Bank 2020b). The World Bank Group’s FCV strategy, endorsed by the Board of Executive Directors on February 25, 2020, recognizes the many challenges facing private investments in fragile and conflict-affected situations (FCS) and the need to address them. These challenges include difficult operating environments, higher costs of doing business, skills shortages, the absence of the rule of law, high levels of informality, and poor infrastructure and supply chains (figure 1.1). The strategy states that FCS need a “development approach that catalyzes private sector development to complement public efforts” (World Bank 2019e, 6).

Figure 1.1. Leading Constraints to the Private Sector in FCS and Non-FCS Countries

Figure 1.1. Leading Constraints to the Private Sector in FCS and Non-FCS Countries

Source: World Bank and Independent Evaluation Group calculations.

Note: FCS = fragile and conflict-affected situations.

FCS countries are underserviced by foreign direct investment (FDI) flows. FDI inflows have declined since 2012, driven by a reduction of investments in some resource-rich countries, and currently remain far below official development assistance and remittances as a source of external financing (figure 1.2).3 FDI is a less-prominent source of external financing in FCS compared with developing countries overall (1.5 percent of gross domestic product in 2010–20 in FCS and 2.5 percent of gross domestic product in non-FCS). Although FCS economies represent 5.8 percent of developing world gross domestic product, they receive only 3.6 percent of FDI flows. Among FCS, FDI flows are concentrated among the top recipients (the top six FCS countries account for 75 percent of net FDI flows to FCS).4

Figure 1.2. Foreign Direct Investment Flows to FCS

Figure 1.2. Foreign Direct Investment Flows to FCS

Sources: World Development Indicators database; Independent Evaluation Group staff calculations.

Note: Non-FCS includes both International Bank for Reconstruction and Development and International Development Association FCS countries. FCS = fragile and conflict-affected situations; FDI = foreign direct investment; GDP = gross domestic product; ODA = official development assistance.

The International Finance Corporation (IFC) and the Multilateral Investment Guarantee Agency (MIGA) have set ambitious corporate targets for scaling up investments in International Development Association (IDA) and FCS countries without a separate target for FCS countries. Supporting investment in FCS has been an IFC corporate priority since 2009, and it adopted an FCS strategy in 2012. IFC has refined its approach over the past decade, introduced several initiatives and instruments to support its engagement in FCS, and expanded its engagements into new areas, such as forced displacement. As part of the 2018 capital increase package, IFC committed to delivering two targets by 2030: 40 percent of its overall business program in IDA and FCS countries and 15–20 percent in low-income IDA and IDA FCS countries (IFC 2019c). IFC’s corporate strategies have also identified priority areas, such as infrastructure, agriculture, and financial and social inclusion in FCS.

FCS countries have been a strategic priority for MIGA since 2005,5 and it seeks to increase the focus on FCS in its current strategy for fiscal years (FY)21–23. The FY12–14 MIGA strategy justified its focus on conflict-affected countries by the low levels of FDI and noted that the lack of strong governments often makes the private sector the best suited to providing crucial services in these countries. By supporting FDI in conflict-affected countries, MIGA was expected to provide demonstration effects, especially to other political risk insurance (PRI) providers that perceived risks in these contexts are too high. The FY15–17 strategy reaffirmed MIGA’s commitment to supporting conflict-affected and postconflict situations and added that these countries are high risk and “fragile.” MIGA aimed to restore investor confidence to help increase private capital flows and encourage new investments by supporting FDI. Its FY18–20 strategy aimed to grow business in FCS to “have impact where private political risk insurers are unwilling to go” (MIGA 2017, 2). The FY21–23 MIGA strategy continues the focus on FCS countries, combined with its emphasis on IDA countries, with a target to increase the share of MIGA guarantees in IDA17 (the 17th Replenishment of IDA) and FCS countries to an average of 30 to 33 percent during FY21–23. Several initiatives related to the implementation of the World Bank Group FCV strategy underpin the current MIGA strategy, including product adaptation, increasing collaboration with the other Bank Group institutions, leveraging blended finance, helping smaller clients meet environmental and social (E&S) standards, and enhancing its conflict sensitivity analysis (MIGA 2020).6

Evaluation Motivation and Objectives

This evaluation seeks to inform the implementation of the World Bank Group FCV strategy and IFC’s and MIGA’s commitments to scale up investments in FCS. As the Bank Group is implementing its first FCV strategy (2020–25), this evaluation seeks to gauge the effectiveness of and develop lessons from efforts to enhance the range of IFC and MIGA initiatives to scale up and improve sustainable private investments in FCS under the capital increase package and IFC’s and MIGA’s strategies.

The evaluation’s objective is to assess how effectively IFC and MIGA have supported sustainable private investment in FCS countries and derive lessons from their experiences. The evaluation assesses IFC’s and MIGA’s effectiveness in scaling up investments in FCS and the outcomes of IFC and MIGA interventions, approaches, and instruments to support private investment in FCS. It focuses on IFC investments, MIGA guarantees, and IFC advisory services to firms.7 The intent is to assess institution-specific issues such as instrument fit, risk management and tolerance, staffing and incentives, and several FCS-specific initiatives and new approaches, such as the Conflict Affected States in Africa (CASA) initiative and the IDA Private Sector Window (PSW). The evaluation also reviews and synthesizes approaches and experiences of comparator institutions.

The evaluation builds on and expands recent Independent Evaluation Group (IEG) evaluative work. It builds on and reflects findings from recent and parallel IEG studies, including an early-stage assessment of the Bank Group’s experience with the PSW, an IFC in FCS synthesis, a cluster note on IFC’s blended finance operations, and a cluster note on IFC in FCS Project Performance Assessment Reports. This evaluation adds insights from country and project cases, distilling new findings and adding nuance to existing ones based on deeper analysis of contextual factors. It expands the knowledge base on MIGA. It also contributes insights on issues identified as critical to IFC’s and MIGA’s implementation of their FCV strategies, including human resources, financial and risk implications, and approaches deployed in FCS.

Methodology and Scope

The evaluation tries to answer the following question: To what extent have IFC and MIGA contributed to development progress by supporting private investment in FCS? This main question includes the following subquestions:

- To what extent have IFC and MIGA instruments been effective in scaling up private investment in FCS?

- How effectively have investments supported by IFC and MIGA delivered development impact in FCS countries and contributed to the financial objectives of the two institutions?

- Which factors have enabled or constrained IFC’s and MIGA’s effectiveness in supporting private investment and development impact in FCS?8

- What are the lessons and implications for scaling up sustainable investment in FCS?

The conceptual framework for the evaluation outlines the links among outcomes, impacts, and the factors affecting them (appendix A). IFC’s and MIGA’s mechanisms and business models (internal factors) shape and support their outcomes and impacts (effectiveness) while addressing the risks and constraints associated with FCS countries and clients (external factors).

The evaluation covers all FCS-relevant activities included in IFC’s and MIGA’s corporate strategies, complementary World Bank interventions as part of the analysis of Bank Group collaboration, and a qualitative analysis of comparator development institutions. First, the evaluation covers all IFC and MIGA instruments during FY10–21 that support private investment in FCS directly, including (i) IFC investment services, (ii) IFC advisory services to private firms in FCS, and (iii) MIGA guarantees. Second, in the country case studies, the evaluation also covers World Bank interventions and IFC advisory services to governments that relate directly to generating private investment.

The concepts used by Bank Group institutions to define FCS are not fully consistent. IEG identified and analyzed the commitments and guarantee volume using the World Bank Harmonized List of Fragile Situations and since FY20, the List of Fragile and Conflict-Affected Situations, due to its methodological rigor and to ensure consistency and comparability of data when assessing the three Bank Group institutions.9 IFC and MIGA have separately adopted a practice of extending the World Bank (harmonized) FCS list by three fiscal years. Finally, both IFC and MIGA track their corporate commitments combining IDA17-eligible and FCS countries.

Evaluation Design

The evaluation is based on a multilevel analysis and derives its findings through the triangulation of several sources of evidence. It conducts analysis on three levels: total portfolio, country (case studies for seven selected countries), and project (an in-depth analysis of 12 projects aligned with the seven country case studies). Appendix A provides additional details on the methodology, the different evaluation components, and the selected country cases and interventions.

The evaluation also reflects complementary background work covering several dimensions of IFC’s and MIGA’s business models and modalities of client engagement in FCS. These dimensions include a review of staffing, human resource policies, and incentives in FCS; an assessment of the CASA initiative; a benchmarking of comparator development finance institutions (DFIs); an analysis of support to gender in FCS; and a review of financial and risk implications for IFC.

This report is organized as follows: Chapter 2 discusses the effectiveness of IFC’s and MIGA’s engagements in FCS. Chapter 3 explores issues and challenges regarding IFC’s and MIGA’s potential to scale up their investment volumes and achieve development impact in FCS. Chapter 4 provides conclusions and recommendations.

- The World Bank Group uses two terms related to fragility and conflict. “Fragile and conflict-affected situations (FCS) refers to a group of countries included in the Harmonized List of Fragile Situations” (appendix D), whereas “fragility, conflict, and violence” refers to a set of vulnerabilities, irrespective of whether a country is classified as FCS (including instances of subnational conflict, forced displacement, and urban violence). Consistent with the operational practice of the International Finance Corporation (IFC) and the Multilateral Investment Guarantee Agency (MIGA), this evaluation refers to the FCS group of countries unless otherwise indicated.

- The services provision by the private sector has two aspects: direct (services provided by the private sector) and indirect (through taxes collected by the government for the provision of essential services).

- Data are based on FCS country classification in fiscal year (FY)19.

- These include the Republic of Congo, Nigeria, Lebanon, Mozambique, Myanmar, and the Democratic Republic of Congo.

- MIGA’s earlier strategies did not use the term FCS. The MIGA FY05–08 Strategy identified the support for cross-border investments in conflict-affected environments and frontier markets and for infrastructure as well as South-South investments as its operational priorities. In its FY09–11 Operational Priorities, MIGA identified support to foreign investments in postconflict countries support for International Development Association (IDA) countries, complex projects (e.g., infrastructure and extractive industries), and South-South investments as its four operational priorities. MIGA’s FY12–14 Strategic Directions reiterated the same four strategic areas as in the previous strategies. MIGA’s FY15–17 Strategic Directions continued to use the term “conflict-affected situations” as one of its focus areas in addition to IDA countries, transformational projects, energy efficiency and climate change, and middle-income countries. It was in MIGA’s FY18–20 Strategy and Business Outlook that the term “FCS” was used as one of MIGA’s three priority areas—the other areas were IDA countries and climate change and energy efficiency. Most recently, in its FY21–23 Strategy and Business Outlook, MIGA committed to increase its guarantees in IDA and FCS countries combined to an average of 30–33 percent during the period.

- The strategy for FY21–23 outlines the following aspects of MIGA’s business model in IDA FCS: (i) through Bank Group collaboration and the Cascade approach, leveraging increased upstream engagement with World Bank and IFC for FCS-specific approaches to public and private sector financing and solutions; (ii) leveraging blended finance solutions to expand MIGA’s ability to take greater financial risk by using blended finance from the MIGA Guarantee Facility under IDA’s Private Sector Window in eligible countries and the Conflict-Affected and Fragile Economies Facility in middle-income countries that are also FCS; (iii) exploring options for a facility to help smaller-capacity clients meet environmental and social and integrity standards; (iv) streamlining by potentially scaling up the Small Investment Program and simplifying approval for smaller, impactful projects, with broader Board of Executive Directors–delegated authority for select projects; and (v) enhancing conflict sensitivity analysis.

- Advisory services for firms that this evaluation covers include the following institution types: private, publicly listed company; private (unlisted) company; private (unlisted) company going public (before initial public offering); nongovernmental or civil society organization; private (unlisted) company associated with a publicly listed company; and international company.

- Factors include the following: (i) those relating to IFC’s and MIGA’s institutional performance, such as business models, policies, adaptation and selection of instruments, risk tolerance, risk mitigation tools, availability of analytical and diagnostic work, staffing and internal incentives, operational costs, and adequacy and effectiveness of partnerships with other actors and collaboration within the Bank Group; (ii) external factors related to specific country conditions (typologies), country and market risks, and general policy and enabling environment; and (iii) factors related to the availability, type, and quality of private clients (for example, foreign, local, or regional firms; state-owned enterprises).

- For the Harmonized List of Fragile Situations, see appendix D, and for the Classification of Fragile and Conflict-Affected Situations, see https://www.worldbank.org/en/topic/fragility conflictviolence/brief/harmonized-list-of-fragile-situations.